infer

Infer vector autoregression model (VAR) innovations

Description

Tbl2 = infer(Mdl,Tbl1)Tbl2 containing the multivariate

residuals from evaluating the fully specified VAR(p) model

Mdl at the response variables in the table or timetable of

data Tbl1. (since R2022b)

infer selects the variables in Mdl.SeriesNames or all variables in Tbl1. To select different response variables in Tbl1 at which to evaluate the model, use the ResponseVariables name-value argument.

___ = infer(___,

specifies options using one or more name-value arguments in

addition to any of the input argument combinations in previous syntaxes.

Name=Value)infer returns the output argument combination for the

corresponding input arguments. For example, infer(Mdl,Y,Y0=PS,X=Exo) computes the

residuals of the VAR(p) model Mdl at the

matrix of response data Y, and specifies the matrix of presample

response data PS and the matrix of exogenous predictor data

Exo.

Supply all input data using the same data type. Specifically:

If you specify the numeric matrix

Y, optional data sets must be numeric arrays and you must use the appropriate name-value argument. For example, to specify a presample, set theY0name-value argument to a numeric matrix of presample data.If you specify the table or timetable

Tbl1, optional data sets must be tables or timetables, respectively, and you must use the appropriate name-value argument. For example, to specify a presample, set thePresamplename-value argument to a table or timetable of presample data.

Examples

Fit a VAR(4) model to the consumer price index (CPI) and unemployment rate data in a matrix. Then, infer the model innovations (residuals) from the estimated model.

Load the Data_USEconModel data set.

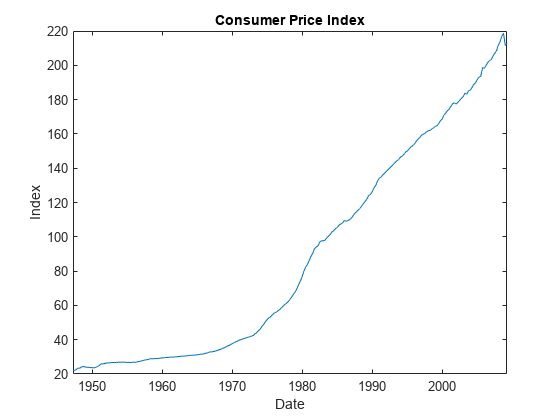

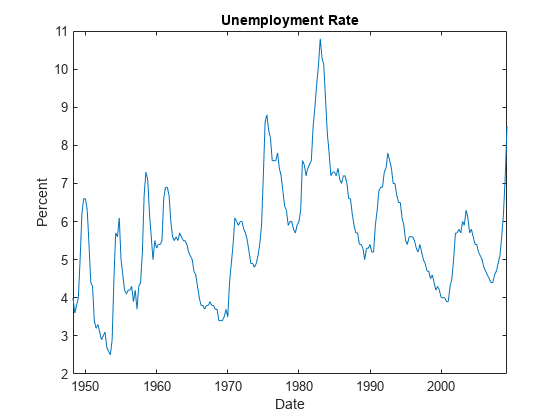

load Data_USEconModelPlot the two series on separate plots.

figure plot(DataTimeTable.Time,DataTimeTable.CPIAUCSL) title("Consumer Price Index") ylabel("Index") xlabel("Date")

figure plot(DataTimeTable.Time,DataTimeTable.UNRATE) title("Unemployment Rate") ylabel("Percent") xlabel("Date")

Stabilize the CPI by converting it to a series of growth rates. Synchronize the two series by removing the first observation from the unemployment rate series.

rcpi = price2ret(DataTimeTable.CPIAUCSL); unrate = DataTimeTable.UNRATE(2:end);

Create a default VAR(4) model by using the shorthand syntax.

Mdl = varm(2,4);

Estimate the model using the entire data set.

EstMdl = estimate(Mdl,[rcpi unrate]);

EstMdl is a fully specified, estimated varm model object.

Infer innovations from the estimated model. Supply the same response data that the model was fit to as a numeric matrix.

E = infer(EstMdl,[rcpi unrate]);

E is a 241-by-2 matrix of inferred innovations. The first and second columns contain the residuals corresponding to the CPI growth rate and unemployment rate, respectively.

Alternatively, you can return residuals when you call estimate by supplying an output variable in the fourth position.

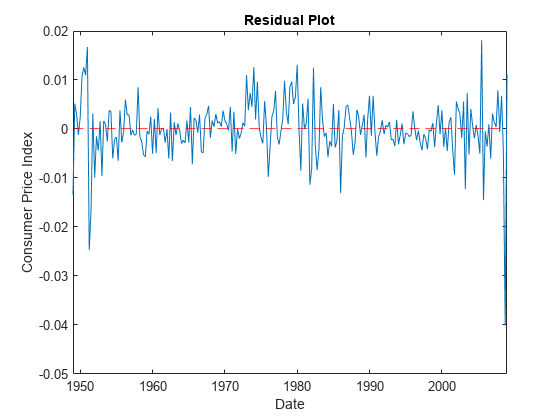

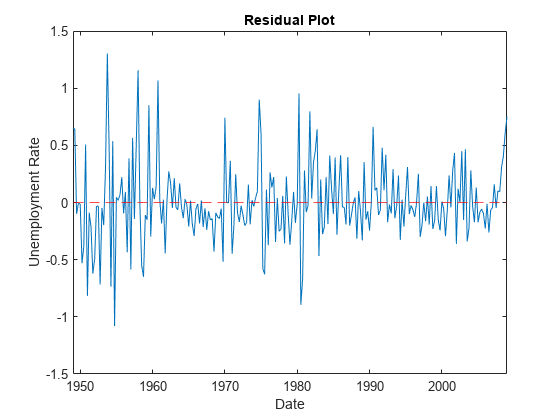

Plot the residuals on separate plots. Synchronize the residuals with the dates by removing any missing observations from the data and removing the first Mdl.P dates.

idx = all(~isnan([rcpi unrate]),2); datesr = DataTimeTable.Time(idx); figure plot(datesr((Mdl.P + 1):end),E(:,1)); ylabel("Consumer Price Index") xlabel("Date") title("Residual Plot") hold on yline(0,"r--"); hold off

figure plot(datesr((Mdl.P + 1):end),E(:,2)) ylabel("Unemployment Rate") xlabel("Date") title("Residual Plot") hold on yline(0,"r--"); hold off

The residuals corresponding to the CPI growth rate exhibit heteroscedasticity because the series appears to cycle through periods of higher and lower variance.

Since R2022b

Fit a VAR(4) model to the consumer price index (CPI) and unemployment rate data in a timetable. Then, infer the model innovations (residuals) from the estimated model.

Load and Preprocess Data

Load the Data_USEconModel data set. Compute the CPI growth rate. Because the growth rate calculation consumes the earliest observation, include the rate variable in the timetable by prepending the series with NaN.

load Data_USEconModel

DataTimeTable.RCPI = [NaN; price2ret(DataTimeTable.CPIAUCSL)];

numobs = height(DataTimeTable)numobs = 249

Prepare Timetable for Estimation

When you plan to supply a timetable directly to estimate, you must ensure it has all the following characteristics:

All selected response variables are numeric and do not contain any missing values.

The timestamps in the

Timevariable are regular, and they are ascending or descending.

Remove all missing values from the table, relative to the CPI rate (RCPI) and unemployment rate (UNRATE) series.

varnames = ["RCPI" "UNRATE"]; DTT = rmmissing(DataTimeTable,DataVariables=varnames); numobs = height(DTT)

numobs = 245

rmmissing removes the four initial missing observations from the DataTimeTable to create a sub-table DTT. The variables RCPI and UNRATE of DTT do not have any missing observations.

Determine whether the sampling timestamps have a regular frequency and are sorted.

areTimestampsRegular = isregular(DTT,"quarters")areTimestampsRegular = logical

0

areTimestampsSorted = issorted(DTT.Time)

areTimestampsSorted = logical

1

areTimestampsRegular = 0 indicates that the timestamps of DTT are irregular. areTimestampsSorted = 1 indicates that the timestamps are sorted. Macroeconomic series in this example are timestamped at the end of the month. This quality induces an irregularly measured series.

Remedy the time irregularity by shifting all dates to the first day of the quarter.

dt = DTT.Time; dt = dateshift(dt,"start","quarter"); DTT.Time = dt; areTimestampsRegular = isregular(DTT,"quarters")

areTimestampsRegular = logical

1

DTT is regular with respect to time.

Create Model Template for Estimation

Create a default VAR(4) model by using the shorthand syntax. Specify the response variable names.

Mdl = varm(2,4); Mdl.SeriesNames = varnames;

Fit Model to Data

Estimate the model. Pass the entire timetable DTT. By default, estimate selects the response variables in Mdl.SeriesNames to fit to the model. Alternatively, you can use the ResponseVariables name-value argument.

EstMdl = estimate(Mdl,DTT);

Compute Residuals

Infer innovations from the estimated model. Supply the same response data that the model was fit to as a timetable. By default, infer selects the variables to use from EstMdl.SeriesNames.

Tbl = infer(EstMdl,DTT); head(Tbl)

Time COE CPIAUCSL FEDFUNDS GCE GDP GDPDEF GPDI GS10 HOANBS M1SL M2SL PCEC TB3MS UNRATE RCPI RCPI_Residuals UNRATE_Residuals

_____ _____ ________ ________ ____ _____ ______ ____ ____ ______ ____ ____ _____ _____ ______ __________ ______________ ________________

Q1-49 144.1 23.91 NaN 45.6 270 16.531 40.9 NaN 53.961 NaN NaN 177 1.17 5 -0.0058382 -0.013422 0.64674

Q2-49 141.9 23.92 NaN 47.3 266.2 16.35 34 NaN 53.058 NaN NaN 178.6 1.17 6.2 0.00041815 0.0051673 0.6439

Q3-49 141 23.75 NaN 47.2 267.7 16.256 37.3 NaN 52.501 NaN NaN 178 1.07 6.6 -0.0071324 0.0030175 -0.099092

Q4-49 140.5 23.61 NaN 46.6 265.2 16.272 35.2 NaN 52.291 NaN NaN 180.4 1.1 6.6 -0.0059122 -0.001196 -0.0066535

Q1-50 144.6 23.64 NaN 45.6 275.2 16.222 44.4 NaN 52.696 NaN NaN 183.1 1.12 6.3 0.0012698 0.0024607 -0.013354

Q2-50 150.6 23.88 NaN 46.1 284.6 16.286 49.9 NaN 53.997 NaN NaN 187 1.15 5.4 0.010101 0.010823 -0.53098

Q3-50 159 24.34 NaN 45.9 302 16.63 56.1 NaN 55.7 NaN NaN 200.7 1.3 4.4 0.01908 0.012566 -0.38177

Q4-50 166.9 24.98 NaN 49.5 313.4 16.95 65.9 NaN 56.213 NaN NaN 198.1 1.34 4.3 0.025954 0.010998 0.50761

size(Tbl)

ans = 1×2

241 17

Tbl is a 241-by-17 timetable of variables in DTT and estimated model residuals, RCPI_Residuals and UNRATE_Residuals.

Alternatively, you can return residuals when you call estimate by supplying an output variable in the fourth position.

Since R2022b

Estimate a VAR(4) model of the consumer price index (CPI), the unemployment rate, and the gross domestic product (GDP). Include a linear regression component containing the current quarter and the last four quarters of government consumption expenditures and investment (GCE). Infer model innovations.

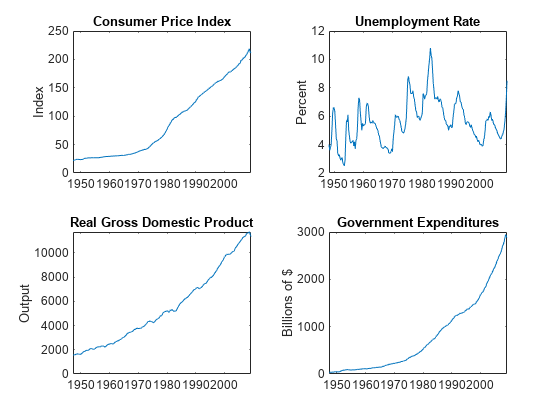

Load the Data_USEconModel data set. Compute the real GDP.

load Data_USEconModel

DataTimeTable.RGDP = DataTimeTable.GDP./DataTimeTable.GDPDEF*100;Plot all variables on separate plots.

figure tiledlayout(2,2) nexttile plot(DataTimeTable.Time,DataTimeTable.CPIAUCSL); ylabel("Index") title("Consumer Price Index") nexttile plot(DataTimeTable.Time,DataTimeTable.UNRATE); ylabel("Percent") title("Unemployment Rate") nexttile plot(DataTimeTable.Time,DataTimeTable.RGDP); ylabel("Output") title("Real Gross Domestic Product") nexttile plot(DataTimeTable.Time,DataTimeTable.GCE); ylabel("Billions of $") title("Government Expenditures")

Stabilize the CPI, GDP, and GCE by converting each to a series of growth rates. Synchronize the unemployment rate series with the others by removing its first observation.

varnames = ["CPIAUCSL" "RGDP" "GCE"]; DTT = varfun(@price2ret,DataTimeTable,InputVariables=varnames); DTT.Properties.VariableNames = varnames; DTT.UNRATE = DataTimeTable.UNRATE(2:end);

Make the time base regular.

dt = DTT.Time; dt = dateshift(dt,"start","quarter"); DTT.Time = dt;

Expand the GCE rate series to a matrix that includes the first lagged series through the fourth lag series.

RGCELags = lagmatrix(DTT,1:4,DataVariables="GCE");

DTT = [DTT RGCELags];

DTT = rmmissing(DTT);Create a default VAR(4) model by using the shorthand syntax. Specify the response variable names.

Mdl = varm(3,4); Mdl.SeriesNames = ["CPIAUCSL" "UNRATE" "RGDP"];

Estimate the model using the entire sample. Specify the GCE and its lags as exogenous predictor data for the regression component.

prednames = contains(DTT.Properties.VariableNames,"GCE");

EstMdl = estimate(Mdl,DTT,PredictorVariables=prednames);Infer innovations from the estimated model. Supply the predictor data. Return the loglikelihood objective function value.

[Tbl,logL] = infer(EstMdl,DTT,PredictorVariables=prednames); size(Tbl)

ans = 1×2

240 11

head(Tbl)

Time CPIAUCSL RGDP GCE UNRATE Lag1GCE Lag2GCE Lag3GCE Lag4GCE CPIAUCSL_Residuals UNRATE_Residuals RGDP_Residuals

_____ __________ __________ __________ ______ __________ __________ __________ __________ __________________ ________________ ______________

Q1-49 0.00041815 -0.0031645 0.036603 6.2 0.047147 0.04948 0.04193 0.054347 0.0053457 0.6564 -0.0053201

Q2-49 -0.0071324 0.011385 -0.0021164 6.6 0.036603 0.047147 0.04948 0.04193 0.0088626 -0.034796 0.010153

Q3-49 -0.0059122 -0.010366 -0.012793 6.6 -0.0021164 0.036603 0.047147 0.04948 0.0029402 0.11695 -0.02318

Q4-49 0.0012698 0.040091 -0.021693 6.3 -0.012793 -0.0021164 0.036603 0.047147 0.0040774 -0.2343 0.026583

Q1-50 0.010101 0.029649 0.010905 5.4 -0.021693 -0.012793 -0.0021164 0.036603 0.0046233 -0.18043 0.0091538

Q2-50 0.01908 0.03844 -0.0043478 4.4 0.010905 -0.021693 -0.012793 -0.0021164 0.015141 -0.34049 0.019797

Q3-50 0.025954 0.017994 0.075508 4.3 -0.0043478 0.010905 -0.021693 -0.012793 0.0041785 0.87368 -0.011263

Q4-50 0.035395 0.01197 0.14807 3.4 0.075508 -0.0043478 0.010905 -0.021693 0.011772 -0.49694 -0.0044563

logL

logL = 1.7056e+03

Tbl is a 240-by-11 timetable of data and inferred innovations from the estimated model (residuals).

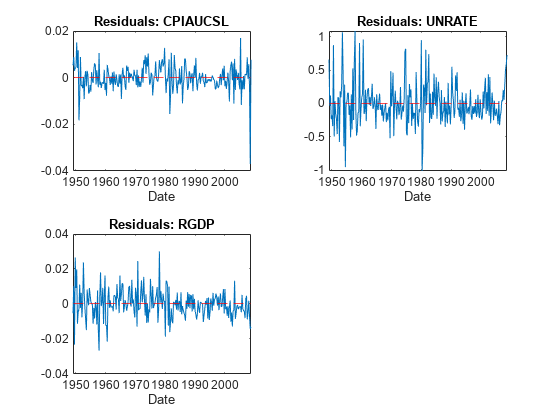

Plot the residuals on separate plots.

idx = endsWith(Tbl.Properties.VariableNames,"_Residuals"); resvars = Tbl.Properties.VariableNames(idx); titles = "Residuals: " + EstMdl.SeriesNames; figure tiledlayout(2,2) for j = 1:Mdl.NumSeries nexttile plot(Tbl.Time,Tbl{:,resvars(j)}); xlabel("Date"); title(titles(j)); hold on yline(0,"r--"); hold off end

The residuals corresponding to the CPI and GDP growth rates exhibit heteroscedasticity because the CPI series appears to cycle through periods of higher and lower variance. Also, the first half of the GDP series seems to have higher variance than the latter half.

Input Arguments

Name-Value Arguments

Output Arguments

Algorithms

Suppose Y, Y0, and X are the

response, presample response, and predictor data specified by the numeric data inputs in

Y, Y0, and X, or the

selected variables from the input tables or timetables Tbl1 and

Presample.

inferinfers innovations by evaluating the VAR modelMdl, specifically,inferuses this process to determine the time origin t0 of models that include linear time trends.If you do not specify

Y0, then t0 = 0.Otherwise,

infersets t0 tosize(Y0,1)–Mdl.P. Therefore, the times in the trend component are t = t0 + 1, t0 + 2,..., t0 +numobs, wherenumobsis the effective sample size (size(Y,1)afterinferremoves missing values). This convention is consistent with the default behavior of model estimation in whichestimateremoves the firstMdl.Presponses, reducing the effective sample size. Althoughinferexplicitly uses the firstMdl.Ppresample responses inY0to initialize the model, the total number of observations inY0andY(excluding missing values) determines t0.

References

[1] Hamilton, James D. Time Series Analysis. Princeton, NJ: Princeton University Press, 1994.

[2] Johansen, S. Likelihood-Based Inference in Cointegrated Vector Autoregressive Models. Oxford: Oxford University Press, 1995.

[3] Juselius, K. The Cointegrated VAR Model. Oxford: Oxford University Press, 2006.

[4] Lütkepohl, H. New Introduction to Multiple Time Series Analysis. Berlin: Springer, 2005.