Fit VAR Model of CPI and Unemployment Rate

This example shows how to estimate the parameters of a VAR(4) model. The response series are quarterly measures of the consumer price index (CPI) and the unemployment rate.

Load the Data_USEconModel data set.

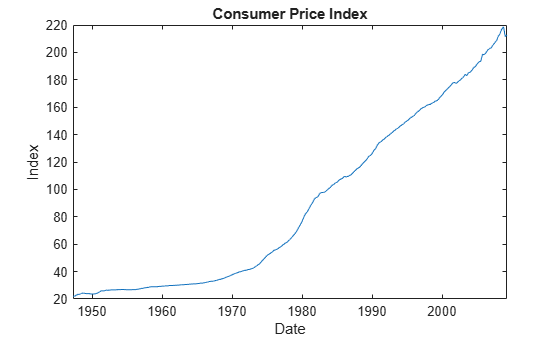

load Data_USEconModelPlot the two series on separate plots.

figure; plot(DataTimeTable.Time,DataTimeTable.CPIAUCSL); title('Consumer Price Index') ylabel('Index') xlabel('Date')

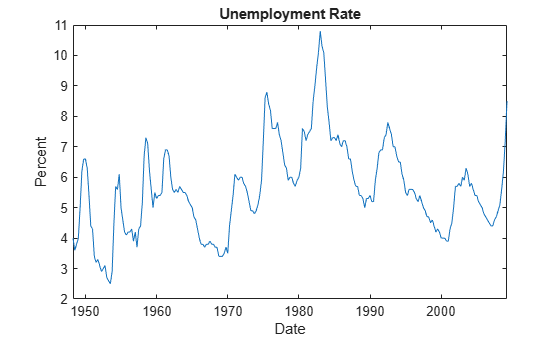

figure; plot(DataTimeTable.Time,DataTimeTable.UNRATE); title('Unemployment Rate') ylabel('Percent') xlabel('Date')

The CPI appears to grow exponentially.

Stabilize the CPI by converting it to a series of growth rates. Synchronize the two series by removing the first observation from the unemployment rate series.

rcpi = price2ret(DataTimeTable.CPIAUCSL); unrate = DataTimeTable.UNRATE(2:end);

Create a default VAR(4) model using the shorthand syntax.

Mdl = varm(2,4)

Mdl =

varm with properties:

Description: "2-Dimensional VAR(4) Model"

SeriesNames: "Y1" "Y2"

NumSeries: 2

P: 4

Constant: [2×1 vector of NaNs]

AR: {2×2 matrices of NaNs} at lags [1 2 3 ... and 1 more]

Trend: [2×1 vector of zeros]

Beta: [2×0 matrix]

Covariance: [2×2 matrix of NaNs]

Mdl is a varm model object. It serves as a template for model estimation. MATLAB� considers any NaN values as unknown parameter values to be estimated. For example, the Constant property is a 2-by-1 vector of NaN values. Therefore, model constants are model parameters to be estimated.

Fit the model to the data.

EstMdl = estimate(Mdl,[rcpi unrate])

EstMdl =

varm with properties:

Description: "AR-Stationary 2-Dimensional VAR(4) Model"

SeriesNames: "Y1" "Y2"

NumSeries: 2

P: 4

Constant: [0.00171639 0.316255]'

AR: {2×2 matrices} at lags [1 2 3 ... and 1 more]

Trend: [2×1 vector of zeros]

Beta: [2×0 matrix]

Covariance: [2×2 matrix]

EstMdl is a varm model object. EstMdl is structurally the same as Mdl, but all parameters are known. To inspect the estimated parameters, you can display them using dot notation.

Display the coefficient of the first lag term.

EstMdl.AR{1}ans = 2×2

0.3090 -0.0032

-4.4834 1.3433

Display an estimation summary including all parameters, standard errors, and *p-*values for testing the null hypothesis that the coefficient is 0.

summarize(EstMdl)

AR-Stationary 2-Dimensional VAR(4) Model

Effective Sample Size: 241

Number of Estimated Parameters: 18

LogLikelihood: 811.361

AIC: -1586.72

BIC: -1524

Value StandardError TStatistic PValue

___________ _____________ __________ __________

Constant(1) 0.0017164 0.0015988 1.0735 0.28303

Constant(2) 0.31626 0.091961 3.439 0.0005838

AR{1}(1,1) 0.30899 0.063356 4.877 1.0772e-06

AR{1}(2,1) -4.4834 3.6441 -1.2303 0.21857

AR{1}(1,2) -0.0031796 0.0011306 -2.8122 0.004921

AR{1}(2,2) 1.3433 0.065032 20.656 8.546e-95

AR{2}(1,1) 0.22433 0.069631 3.2217 0.0012741

AR{2}(2,1) 7.1896 4.005 1.7951 0.072631

AR{2}(1,2) 0.0012375 0.0018631 0.6642 0.50656

AR{2}(2,2) -0.26817 0.10716 -2.5025 0.012331

AR{3}(1,1) 0.35333 0.068287 5.1742 2.2887e-07

AR{3}(2,1) 1.487 3.9277 0.37858 0.705

AR{3}(1,2) 0.0028594 0.0018621 1.5355 0.12465

AR{3}(2,2) -0.22709 0.1071 -2.1202 0.033986

AR{4}(1,1) -0.047563 0.069026 -0.68906 0.49079

AR{4}(2,1) 8.6379 3.9702 2.1757 0.029579

AR{4}(1,2) -0.00096323 0.0011142 -0.86448 0.38733

AR{4}(2,2) 0.076725 0.064088 1.1972 0.23123

Innovations Covariance Matrix:

0.0000 -0.0002

-0.0002 0.1167

Innovations Correlation Matrix:

1.0000 -0.0925

-0.0925 1.0000