Create Regression Models with ARIMA Errors

Default Regression Model with ARIMA Errors Specifications

Regression models with ARIMA errors have the following form (in lag operator notation):

where

t = 1,...,T.

yt is the response series.

Xt is row t of X, which is the matrix of concatenated predictor data vectors. That is, Xt is observation t of each predictor series.

c is the regression model intercept.

β is the regression coefficient.

ut is the disturbance series.

εt is the innovations series.

which is the degree p, nonseasonal autoregressive polynomial.

which is the degree ps, seasonal autoregressive polynomial.

which is the degree D, nonseasonal integration polynomial.

which is the degree s, seasonal integration polynomial.

which is the degree q, nonseasonal moving average polynomial.

which is the degree qs, seasonal moving average polynomial.

For simplicity, use the shorthand notation Mdl =

regARIMA(p,D,q) to specify a regression model with

ARIMA(p,D,q) errors,

where p, D, and q are

nonnegative integers. Mdl has the following default

properties.

| Property Name | Property Data Type |

|---|---|

AR | Length p cell vector of

NaNs |

Beta | Empty vector [] of regression

coefficients, corresponding to the predictor series |

D | Nonnegative scalar, corresponding to D |

Distribution | "Gaussian", corresponding to the

distribution of

εt |

Intercept | NaN, corresponding to

c |

MA | Length q cell vector of

NaNs |

P | Number of AR terms plus degree of integration, p + D |

Q | Number of MA terms, q |

SAR | Empty cell vector |

SMA | Empty cell vector |

Variance | NaN, corresponding to the variance of

εt |

Seasonality | 0, corresponding to

s |

If you specify nonseasonal ARIMA errors, then

The properties

DandQare the inputsDandq, respectively.Property

P=p+D, which is the degree of the compound, nonseasonal autoregressive polynomial. In other words,Pis the degree of the product of the nonseasonal autoregressive polynomial, a(L) and the nonseasonal integration polynomial, (1 – L)D.

The values of properties P and

Q indicate how many presample observations the software

requires to initialize the time series.

You can modify the properties of Mdl using dot notation. For

example, Mdl.Variance = 0.5 sets the innovation variance to

0.5.

For maximum flexibility in specifying a regression model with ARIMA errors, use

name-value pair arguments to, for example, set each of the autoregressive parameters

to a value, or specify multiplicative seasonal terms. For example, Mdl =

regARIMA('AR',{0.2 0.1}) defines a regression model with AR(2) errors,

and the coefficients are a1 = 0.2 and

a2 = 0.1.

Specify regARIMA Models Using Name-Value Pair Arguments

You can only specify the nonseasonal autoregressive and moving average polynomial

degrees, and nonseasonal integration degree using the shorthand notation

regARIMA(p,D,q). Some tasks, such as forecasting and

simulation, require you to specify values for parameters. You cannot specify

parameter values using shorthand notation. For maximum flexibility, use name-value

pair arguments to specify regression models with ARIMA errors.

The nonseasonal ARIMA error model might contain the following polynomials:

The degree p autoregressive polynomial a(L) = 1 – a1L – a2L2 –...– apLp. The eigenvalues of a(L) must lie within the unit circle (i.e., a(L) must be a stable polynomial).

The degree q moving average polynomial b(L) = 1 + b1L + b2L2 +...+ bqLq. The eigenvalues of b(L) must lie within the unit circle (i.e., b(L) must be an invertible polynomial).

The degree D nonseasonal integration polynomial is (1 – L)D.

The following table contains the name-value pair arguments that you use to specify the ARIMA error model (i.e., a regression model with ARIMA errors, but without a regression component and intercept):

| (1) |

Name-Value Pair Arguments for Nonseasonal ARIMA Error Models

| Name | Corresponding Model Term(s) in Equation 1 | When to Specify |

|---|---|---|

AR | Nonseasonal AR coefficients: a1, a2,...,ap |

|

ARLags | Lags corresponding to nonzero, nonseasonal AR coefficients |

|

D | Degree of nonseasonal differencing, D |

|

Distribution | Distribution of the innovation process, εt |

|

MA | Nonseasonal MA coefficients: b1, b2,...,bq |

|

MALags | Lags corresponding to nonzero, nonseasonal MA coefficients |

|

Variance | Scalar variance, σ2, of the innovation process, εt | To set equality constraints for

σ2. For

example, for an ARIMA error model with known innovation

variance 0.1, specify |

Use the name-value pair arguments in the following table in conjunction with those in Name-Value Pair Arguments for Nonseasonal ARIMA Error Models to specify the regression components of the regression model with ARIMA errors:

| (2) |

Name-Value Pair Arguments for the Regression Component of the regARIMA Model

| Name | Corresponding Model Term(s) in Equation 2 | When to Specify |

|---|---|---|

Beta | Regression coefficient values corresponding to the predictor series, β |

|

Intercept | Intercept term for the regression model, c |

|

If the time series has seasonality s, then

The degree ps seasonal autoregressive polynomial is A(L) = 1 – A 1L – A2L2 –...– ApsLps.

The degree qs seasonal moving average polynomial is B(L) 1 + B 1L + B2L2 +...+ BqsLqs.

The degree s seasonal integration polynomial is (1 – Ls).

Use the name-value pair arguments in the following table in conjunction with those in tables Name-Value Pair Arguments for Nonseasonal ARIMA Error Models and Name-Value Pair Arguments for the Regression Component of the regARIMA Model to specify the regression model with multiplicative seasonal ARIMA errors:

| (3) |

Name-Value Pair Arguments for Seasonal ARIMA Models

| Argument | Corresponding Model Term(s) in Equation 3 | When to Specify |

|---|---|---|

SAR | Seasonal AR coefficients: A1, A2,...,Aps |

|

SARLags | Lags corresponding to nonzero seasonal AR coefficients, in the periodicity of the responses |

|

SMA | Seasonal MA coefficients: B1, B2,...,Bqs |

|

SMALags | Lags corresponding to the nonzero seasonal MA coefficients, in the periodicity of the responses |

|

Seasonality | Seasonal periodicity, s |

|

Note

You cannot assign values to the properties P and

Q. For multiplicative ARIMA error models,

regARIMAsetsPequal to p + D + ps + s.regARIMAsetsQequal to q + qs

Specify Linear Regression Models Using Econometric Modeler App

You can specify the predictor variables in the regression component, and the error model lag structure and innovation distribution, using the Econometric Modeler app. The app treats all coefficients as unknown and estimable.

At the command line, open the Econometric Modeler app.

econometricModeler

Alternatively, open the app from the apps gallery (see Econometric Modeler).

In the app, you can see all supported models by selecting a time series variable for the response in the Time Series pane. Then, on the Econometric Modeler tab, in the Models section, click the arrow to display the models gallery.

The Regression Models section contains supported regression

models. To specify a multiple linear regression (MLR) model, select

MLR. To specify regression models with ARMA errors,

select RegARMA.

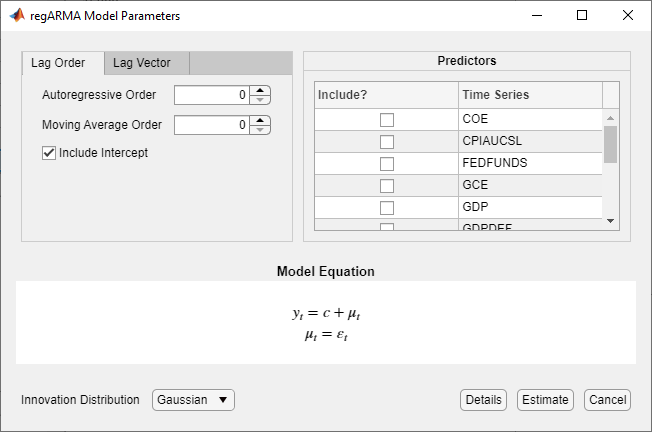

After you select a model, the app displays the

Type Model Parameters dialog

box, where Type is the model type. This figure shows the

RegARMA Model Parameters dialog box.

Adjustable parameters depend on the model Type. In

general, adjustable parameters include:

Predictor variables for the linear regression component, listed in the Predictors section.

For regression models with ARMA errors, you must include at least one predictor in the model. To include a predictor, select the corresponding check box in the Include? column.

For MLR models, you can clear all check boxes in the Include? column. In this case, you can specify a constant mean model (intercept-only model) by selecting the Include Intercept check box. Or, you can specify an error-only model by clearing the Include Intercept check box.

The innovation distribution and nonseasonal lags for the error model, for regression models with ARMA errors.

As you adjust parameter values, the equation in the Model

Equation section changes to match your specifications. Adjustable

parameters correspond to input and name-value pair arguments described in the

previous sections and in the regARIMA reference page.

For more details on specifying models using the app, see Fitting Models to Data and Specifying Univariate Lag Operator Polynomials Interactively.

See Also

Apps

Objects

Topics

- Analyze Time Series Data Using Econometric Modeler

- Specifying Univariate Lag Operator Polynomials Interactively

- Specify Default Regression Model with ARIMA Errors

- Modify regARIMA Model Properties

- Create Regression Models with AR Errors

- Create Regression Models with MA Errors

- Create Regression Models with ARMA Errors

- Create Regression Models with SARIMA Errors

- Specify ARIMA Error Model Innovation Distribution

- Regression Models with Time Series Errors