plot

Visualize prior and posterior densities of Bayesian linear regression model parameters

Syntax

Description

plot( or

PosteriorMdl)plot( plots the posterior or

prior distributions of the parameters in the Bayesian linear regression

model

PriorMdl)PosteriorMdl or PriorMdl, respectively.

plot adds subplots for each parameter to one figure and

overwrites the same figure when you call plot multiple

times.

plot(

plots the posterior and prior distributions in the same subplot.

PosteriorMdl,PriorMdl)plot uses solid blue lines for posterior

densities and dashed red lines for prior densities.

plot(___,

uses any of the input argument combinations in the previous syntaxes and

additional options specified by one or more name-value pair arguments. For

example, you can evaluate the posterior or prior density by supplying values of

β and σ2,

or choose which parameter distributions to include in the figure.Name,Value)

pointsUsed = plot(___)plot

uses to evaluate the densities in the subplots.

[

also returns the values of the evaluated densities.pointsUsed,posteriorDensity,priorDensity]

= plot(___)

If you specify one model, then plot returns the

density values in PosteriorDensity. Otherwise,

plot returns the posterior density values in

PosteriorDensity and the prior density values in

PriorDensity.

[

returns the figure handle of the figure containing the distributions.pointsUsed,posteriorDensity,priorDensity,FigureHandle]

= plot(___)

Examples

Consider the multiple linear regression model that predicts the US real gross national product (GNPR) using a linear combination of industrial production index (IPI), total employment (E), and real wages (WR).

For all , is a series of independent Gaussian disturbances with a mean of 0 and variance .

Assume these prior distributions:

. is a 4-by-1 vector of means, and is a scaled 4-by-4 positive definite covariance matrix.

. and are the shape and scale, respectively, of an inverse gamma distribution.

These assumptions and the data likelihood imply a normal-inverse-gamma conjugate model.

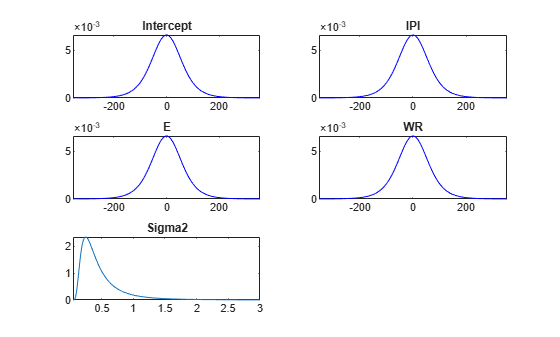

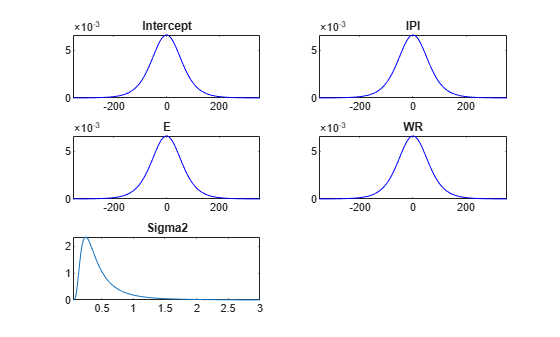

Create a normal-inverse-gamma conjugate prior model for the linear regression parameters. Specify the number of predictors p and the variable names.

p = 3; VarNames = ["IPI" "E" "WR"]; PriorMdl = bayeslm(p,'ModelType','conjugate','VarNames',VarNames);

PriorMdl is a conjugateblm Bayesian linear regression model object representing the prior distribution of the regression coefficients and disturbance variance.

Plot the prior distributions.

plot(PriorMdl);

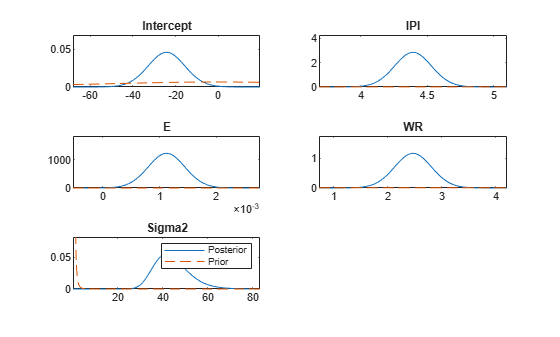

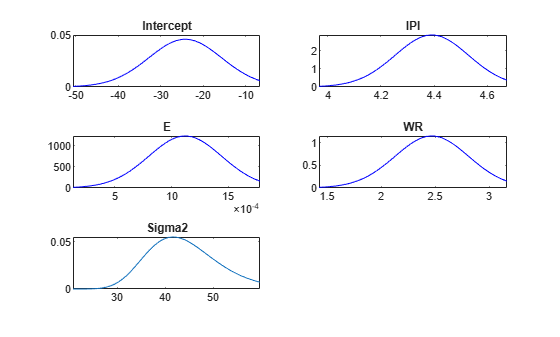

plot plots the marginal prior distributions of the intercept, regression coefficients, and disturbance variance.

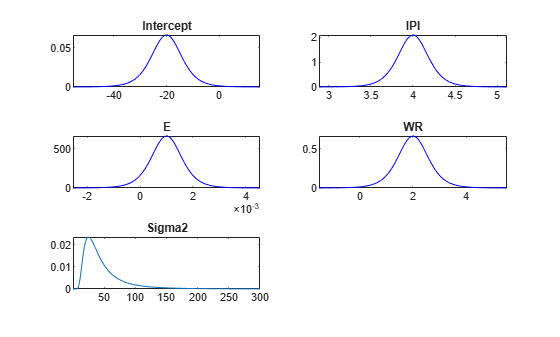

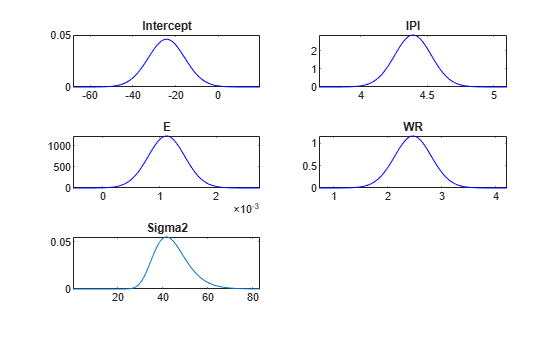

Suppose that the mean of the regression coefficients is and their scaled covariance matrix is

Also, the prior scale of the disturbance variance is 0.01. Specify the prior information using dot notation.

PriorMdl.Mu = [-20; 4; 0.001; 2]; PriorMdl.V = diag([1 0.001 1e-8 0.01]); PriorMdl.B = 0.01;

Request a new figure and plot the prior distribution.

plot(PriorMdl);

plot replaces the current distribution figure with a plot of the prior distribution of the disturbance variance.

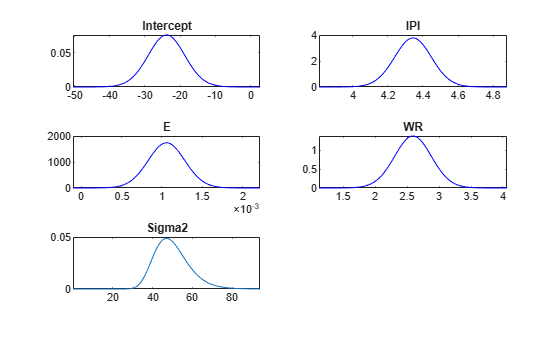

Load the Nelson-Plosser data set, and create variables for the predictor and response data.

load Data_NelsonPlosser

X = DataTable{:,PriorMdl.VarNames(2:end)};

y = DataTable.GNPR;Estimate the posterior distributions.

PosteriorMdl = estimate(PriorMdl,X,y,'Display',false);PosteriorMdl is a conjugateblm model object that contains the posterior distributions of and .

Plot the posterior distributions.

plot(PosteriorMdl);

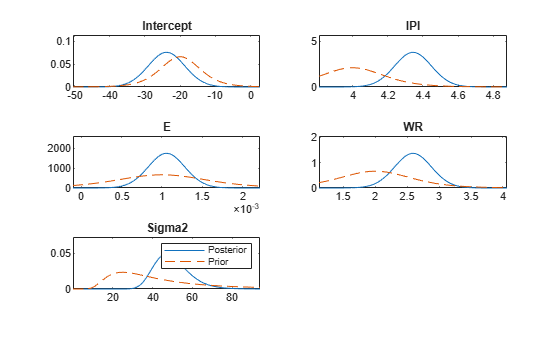

Plot the prior and posterior distributions of the parameters on the same subplots.

plot(PosteriorMdl,PriorMdl);

Consider the regression model in Plot Prior and Posterior Distributions.

Load the Nelson-Plosser data set, create a default conjugate prior model, and then estimate the posterior using the first 75% of the data. Turn off the estimation display.

p = 3; VarNames = ["IPI" "E" "WR"]; PriorMdl = bayeslm(p,'ModelType','conjugate','VarNames',VarNames); load Data_NelsonPlosser X = DataTable{:,PriorMdl.VarNames(2:end)}; y = DataTable.GNPR; d = 0.75; PosteriorMdlFirst = estimate(PriorMdl,X(1:floor(d*end),:),y(1:floor(d*end)),... 'Display',false);

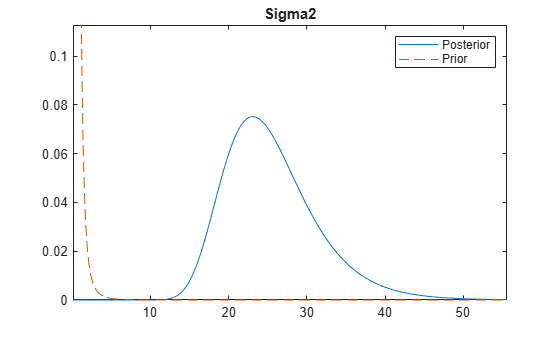

Plot the prior distribution and the posterior distribution of the disturbance variance. Return the figure handle.

[~,~,~,h] = plot(PosteriorMdlFirst,PriorMdl,'VarNames','Sigma2');

h is the figure handle for the distribution plot. If you change the tag name of the figure by changing the Tag property, then the next plot call places all new distribution plots on a different figure.

Change the name of the figure handle to FirstHalfData using dot notation.

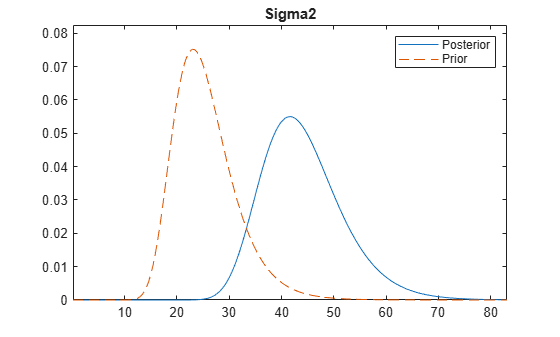

h.Tag = 'FirstHalfData';Estimate the posterior distribution using the rest of the data. Specify the posterior distribution based on the final 25% of the data as the prior distribution.

PosteriorMdl = estimate(PosteriorMdlFirst,X(ceil(d*end):end,:),... y(ceil(d*end):end),'Display',false);

Plot the posterior of the disturbance variance based on half of the data and all the data to a new figure.

plot(PosteriorMdl,PosteriorMdlFirst,'VarNames','Sigma2');

This type of plot shows the evolution of the posterior distribution when you incorporate new data.

Consider the regression model in Plot Prior and Posterior Distributions.

Load the Nelson-Plosser data set and create a default conjugate prior model.

p = 3; VarNames = ["IPI" "E" "WR"]; PriorMdl = bayeslm(p,'ModelType','conjugate','VarNames',VarNames); load Data_NelsonPlosser X = DataTable{:,PriorMdl.VarNames(2:end)}; y = DataTable.GNPR;

Plot the prior distributions. Request the values of the parameters used to create the plots and their respective densities.

[pointsUsedPrior,priorDensities1] = plot(PriorMdl);

pointsUsedPrior is a 5-by-1 cell array of 1-by-1000 numeric vectors representing the values of the parameters that plot uses to plot the corresponding densities. The first element corresponds to the intercept, the next three elements correspond to the regression coefficients, and the last element corresponds to the disturbance variance. priorDensities1 has the same dimensions as pointsUsed and contains the corresponding density values.

Estimate the posterior distribution. Turn off the estimation display.

PosteriorMdl = estimate(PriorMdl,X,y,'Display',false);Plot the posterior distributions. Request the values of the parameters used to create the plots and their respective densities.

[pointsUsedPost,posteriorDensities1] = plot(PosteriorMdl);

pointsUsedPost and posteriorDensities1 have the same dimensions as pointsUsedPrior. The pointsUsedPost output can be different from pointsUsedPrior. posteriorDensities1 contains the posterior density values.

Plot the prior and posterior distributions. Request the values of the parameters used to create the plots and their respective densities.

[pointsUsedPP,posteriorDensities2,priorDensities2] = plot(PosteriorMdl,PriorMdl);

All output values have the same dimensions as pointsUsedPrior. The posteriorDensities2 output contains the posterior density values. The priorDensities2 output contains the prior density values.

Confirm that pointsUsedPP is equal to pointsUsedPost.

compare = @(a,b)sum(a == b) == numel(a); cellfun(compare,pointsUsedPost,pointsUsedPP)

ans = 5×1 logical array

1

1

1

1

1

The points used are equivalent.

Confirm that the posterior densities are the same, but that the prior densities are not.

cellfun(compare,posteriorDensities1,posteriorDensities2)

ans = 5×1 logical array

1

1

1

1

1

cellfun(compare,priorDensities1,priorDensities2)

ans = 5×1 logical array

0

0

0

0

0

When plotting only the prior distribution, plot evaluates the prior densities at points that produce a clear plot of the prior distribution. When plotting both a prior and posterior distribution, plot prefers to plot the posterior clearly. Therefore, plot can determine a different set of points to use.

Consider the regression model in Plot Prior and Posterior Distributions.

Load the Nelson-Plosser data set and create a default conjugate prior model for the regression coefficients and disturbance variance. Then, estimate the posterior distribution and obtain the estimation summary table from summarize.

p = 3; VarNames = ["IPI" "E" "WR"]; PriorMdl = bayeslm(p,'ModelType','conjugate','VarNames',VarNames); load Data_NelsonPlosser X = DataTable{:,PriorMdl.VarNames(2:end)}; y = DataTable.GNPR; PosteriorMdl = estimate(PriorMdl,X,y);

Method: Analytic posterior distributions

Number of observations: 62

Number of predictors: 4

Log marginal likelihood: -259.348

| Mean Std CI95 Positive Distribution

-----------------------------------------------------------------------------------

Intercept | -24.2494 8.7821 [-41.514, -6.985] 0.003 t (-24.25, 8.65^2, 68)

IPI | 4.3913 0.1414 [ 4.113, 4.669] 1.000 t (4.39, 0.14^2, 68)

E | 0.0011 0.0003 [ 0.000, 0.002] 1.000 t (0.00, 0.00^2, 68)

WR | 2.4683 0.3490 [ 1.782, 3.154] 1.000 t (2.47, 0.34^2, 68)

Sigma2 | 44.1347 7.8020 [31.427, 61.855] 1.000 IG(34.00, 0.00069)

summaryTbl = summarize(PosteriorMdl); summaryTbl = summaryTbl.MarginalDistributions;

summaryTbl is a table containing the statistics that estimate displays at the command line.

For each parameter, determine a set of 50 evenly spaced values within three standard deviations of the mean. Put the values into the cells of a 5-by-1 cell vector following the order of the parameters that comprise the rows of the estimation summary table.

Points = cell(numel(summaryTbl.Mean),1); % Preallocation for j = 1:numel(summaryTbl.Mean) Points{j} = linspace(summaryTbl.Mean(j) - 3*summaryTbl.Std(j),... summaryTbl.Mean(j) + 2*summaryTbl.Std(j),50); end

Plot the posterior distributions within their respective intervals.

plot(PosteriorMdl,'Points',Points)

Input Arguments

Name-Value Arguments

Output Arguments

Limitations

Because improper distributions (distributions with densities

that do not integrate to 1) are not well defined, plot

cannot plot them very well.

More About

Version History

Introduced in R2017a

See Also

Objects

conjugateblm|semiconjugateblm|diffuseblm|empiricalblm|customblm|mixconjugateblm|mixsemiconjugateblm|lassoblm