copulapdf

Copula probability density function

Description

Examples

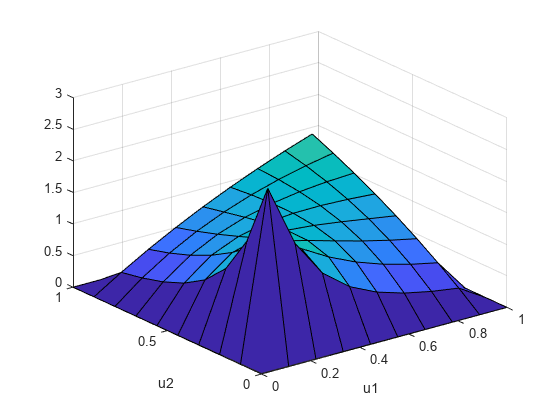

Define two 10-by-10 matrices containing the values at which to compute the pdf.

u = linspace(0,1,10); [u1,u2] = meshgrid(u,u);

Compute the pdf of a Clayton copula that has an alpha parameter equal to 1, at the values in u.

y = copulapdf('Clayton',[u1(:),u2(:)],1);Plot the pdf as a surface, and label the axes.

surf(u1,u2,reshape(y,10,10)) xlabel('u1') ylabel('u2')

Input Arguments

Output Arguments

Version History

Introduced in R2006a