modelCalibration

Compute R-square, RMSE, correlation, and sample mean error of predicted and observed LGDs

Since R2023a

Syntax

Description

CalMeasure = modelCalibration(lgdModel,data)modelCalibration supports comparison against a reference

model and also supports different correlation types. By default,

modelCalibration computes the metrics in the LGD scale. You

can use the ModelLevel name-value pair argument to compute

metrics using the underlying model's transformed scale.

[

specifies options using one or more name-value pair arguments in addition to the

input arguments in the previous syntax.CalMeasure,CalData] = modelCalibration(___,Name,Value)

Examples

This example shows how to use fitLGDModel to fit data with a Regression model and then use modelCalibration to compute the R-Square, RMSE, correlation, and sample mean error of predicted and observed LGDs.

Load Data

Load the loss given default data.

load LGDData.mat

head(data) LTV Age Type LGD

_______ _______ ___________ _________

0.89101 0.39716 residential 0.032659

0.70176 2.0939 residential 0.43564

0.72078 2.7948 residential 0.0064766

0.37013 1.237 residential 0.007947

0.36492 2.5818 residential 0

0.796 1.5957 residential 0.14572

0.60203 1.1599 residential 0.025688

0.92005 0.50253 investment 0.063182

Partition Data

Separate the data into training and test partitions.

rng('default'); % for reproducibility NumObs = height(data); c = cvpartition(NumObs,'HoldOut',0.4); TrainingInd = training(c); TestInd = test(c);

Create Regression LGD Model

Use fitLGDModel to create a Regression model using training data.

lgdModel = fitLGDModel(data(TrainingInd,:),'regression');

disp(lgdModel) Regression with properties:

ResponseTransform: "logit"

BoundaryTolerance: 1.0000e-05

ModelID: "Regression"

Description: ""

UnderlyingModel: [1×1 classreg.regr.CompactLinearModel]

PredictorVars: ["LTV" "Age" "Type"]

ResponseVar: "LGD"

WeightsVar: ""

Display the underlying model.

lgdModel.UnderlyingModel

ans =

Compact linear regression model:

LGD_logit ~ 1 + LTV + Age + Type

Estimated Coefficients:

Estimate SE tStat pValue

________ ________ _______ __________

(Intercept) -4.7549 0.36041 -13.193 3.0997e-38

LTV 2.8565 0.41777 6.8377 1.0531e-11

Age -1.5397 0.085716 -17.963 3.3172e-67

Type_investment 1.4358 0.2475 5.8012 7.587e-09

Number of observations: 2093, Error degrees of freedom: 2089

Root Mean Squared Error: 4.24

R-squared: 0.206, Adjusted R-Squared: 0.205

F-statistic vs. constant model: 181, p-value = 2.42e-104

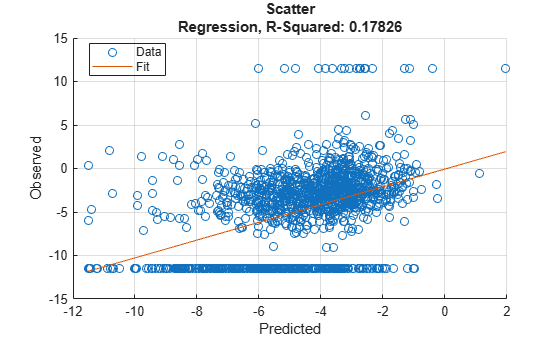

Compute R-Square, RMSE, Correlation, and Sample Mean Error of Predicted and Observed LGDs

Use modelCalibration to compute the RSquared, RMSE, Correlation, and SampleMeanError of the predicted and observed LGDs for the test data set.

[CalMeasure,CalData] = modelCalibration(lgdModel,data(TestInd,:))

CalMeasure=1×4 table

RSquared RMSE Correlation SampleMeanError

________ _______ ___________ _______________

Regression 0.070867 0.25988 0.26621 0.10759

CalData=1394×4 table

Observed Predicted_Regression Residuals_Regression Weights

_________ ____________________ ____________________ _______

0.0064766 0.00091169 0.0055649 1

0.007947 0.0036758 0.0042713 1

0.063182 0.18774 -0.12456 1

0 0.0010877 -0.0010877 1

0.10904 0.011213 0.097823 1

0 0.041992 -0.041992 1

0.89463 0.052947 0.84168 1

0 3.7188e-06 -3.7188e-06 1

0.072437 0.0090124 0.063425 1

0.036006 0.023928 0.012078 1

0 0.0034833 -0.0034833 1

0.39549 0.0065253 0.38896 1

0.057675 0.071956 -0.014281 1

0.014439 0.0061499 0.008289 1

0 0.0012183 -0.0012183 1

0 0.0019828 -0.0019828 1

⋮

Generate a scatter plot of predicted and observed LGDs using modelCalibrationPlot.

modelCalibrationPlot(lgdModel,data(TestInd,:),ModelLevel="underlying")

This example shows how to use fitLGDModel to fit data with a Tobit model and then use modelCalibration to compute R-Square, RMSE, correlation, and sample mean error of predicted and observed LGDs.

Load Data

Load the loss given default data.

load LGDData.mat

head(data) LTV Age Type LGD

_______ _______ ___________ _________

0.89101 0.39716 residential 0.032659

0.70176 2.0939 residential 0.43564

0.72078 2.7948 residential 0.0064766

0.37013 1.237 residential 0.007947

0.36492 2.5818 residential 0

0.796 1.5957 residential 0.14572

0.60203 1.1599 residential 0.025688

0.92005 0.50253 investment 0.063182

Partition Data

Separate the data into training and test partitions.

rng('default'); % for reproducibility NumObs = height(data); c = cvpartition(NumObs,'HoldOut',0.4); TrainingInd = training(c); TestInd = test(c);

Create Tobit LGD Model

Use fitLGDModel to create a Tobit model using training data.

lgdModel = fitLGDModel(data(TrainingInd,:),'tobit');

disp(lgdModel) Tobit with properties:

CensoringSide: "both"

LeftLimit: 0

RightLimit: 1

Weights: [0×1 double]

ModelID: "Tobit"

Description: ""

UnderlyingModel: [1×1 risk.internal.credit.TobitModel]

PredictorVars: ["LTV" "Age" "Type"]

ResponseVar: "LGD"

WeightsVar: ""

Display the underlying model.

disp(lgdModel.UnderlyingModel)

Tobit regression model:

LGD = max(0,min(Y*,1))

Y* ~ 1 + LTV + Age + Type

Estimated coefficients:

Estimate SE tStat pValue

_________ _________ _______ __________

(Intercept) 0.058257 0.027288 2.1349 0.032888

LTV 0.20126 0.03138 6.4136 1.7523e-10

Age -0.095407 0.0072525 -13.155 0

Type_investment 0.10208 0.018069 5.6495 1.8283e-08

(Sigma) 0.29288 0.0057103 51.289 0

Number of observations: 2093

Number of left-censored observations: 547

Number of uncensored observations: 1521

Number of right-censored observations: 25

Log-likelihood: -698.383

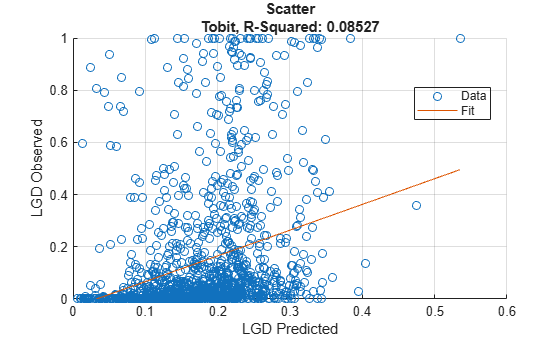

Compute R-Square, RMSE, Correlation, and Sample Mean Error of Predicted and Observed LGDs

Use modelCalibration to compute RSquared, RMSE, Correlation, and SampleMeanError of predicted and observed LGDs for the test data set.

[CalMeasure,CalData] = modelCalibration(lgdModel,data(TestInd,:),CorrelationType="kendall")CalMeasure=1×4 table

RSquared RMSE Correlation SampleMeanError

________ _______ ___________ _______________

Tobit 0.08527 0.23712 0.29964 -0.034412

CalData=1394×4 table

Observed Predicted_Tobit Residuals_Tobit Weights

_________ _______________ _______________ _______

0.0064766 0.087889 -0.081412 1

0.007947 0.12432 -0.11638 1

0.063182 0.32043 -0.25724 1

0 0.093354 -0.093354 1

0.10904 0.16718 -0.058144 1

0 0.22382 -0.22382 1

0.89463 0.23695 0.65768 1

0 0.010234 -0.010234 1

0.072437 0.1592 -0.086761 1

0.036006 0.19893 -0.16292 1

0 0.12764 -0.12764 1

0.39549 0.14568 0.2498 1

0.057675 0.26181 -0.20413 1

0.014439 0.14483 -0.13039 1

0 0.094123 -0.094123 1

0 0.10944 -0.10944 1

⋮

Generate a scatter plot of the predicted and observed LGDs using modelCalibrationPlot.

modelCalibrationPlot(lgdModel,data(TestInd,:))

This example shows how to use fitLGDModel to fit data with a Beta model and then use modelCalibration to compute R-Square, RMSE, correlation, and sample mean error of predicted and observed LGDs.

Load Data

Load the loss given default data.

load LGDData.mat

head(data) LTV Age Type LGD

_______ _______ ___________ _________

0.89101 0.39716 residential 0.032659

0.70176 2.0939 residential 0.43564

0.72078 2.7948 residential 0.0064766

0.37013 1.237 residential 0.007947

0.36492 2.5818 residential 0

0.796 1.5957 residential 0.14572

0.60203 1.1599 residential 0.025688

0.92005 0.50253 investment 0.063182

Partition Data

Separate the data into training and test partitions.

rng('default'); % for reproducibility NumObs = height(data); c = cvpartition(NumObs,'HoldOut',0.4); TrainingInd = training(c); TestInd = test(c);

Create Beta LGD Model

Use fitLGDModel to create a Beta model using training data.

lgdModel = fitLGDModel(data(TrainingInd,:),'Beta');

disp(lgdModel) Beta with properties:

BoundaryTolerance: 1.0000e-05

ModelID: "Beta"

Description: ""

UnderlyingModel: [1×1 risk.internal.credit.BetaModel]

PredictorVars: ["LTV" "Age" "Type"]

ResponseVar: "LGD"

WeightsVar: ""

Display the underlying model.

disp(lgdModel.UnderlyingModel)

Beta regression model:

logit(LGD) ~ 1_mu + LTV_mu + Age_mu + Type_mu

log(LGD) ~ 1_phi + LTV_phi + Age_phi + Type_phi

Estimated coefficients:

Estimate SE tStat pValue

________ ________ _______ __________

(Intercept)_mu -1.3772 0.13201 -10.433 0

LTV_mu 0.6027 0.15087 3.9947 6.7017e-05

Age_mu -0.47464 0.040264 -11.788 0

Type_investment_mu 0.45372 0.085143 5.3289 1.0942e-07

(Intercept)_phi -0.16336 0.12591 -1.2974 0.19463

LTV_phi 0.055886 0.14719 0.37968 0.70422

Age_phi 0.22887 0.040335 5.6743 1.5865e-08

Type_investment_phi -0.14102 0.078155 -1.8044 0.071313

Number of observations: 2093

Log-likelihood: -5291.04

Compute R-Square, RMSE, Correlation, and Sample Mean Error of Predicted and Observed LGDs

Use modelCalibration to compute RSquared, RMSE, Correlation, and SampleMeanError of predicted and observed LGDs for the test data set.

[CalMeasure,CalData] = modelCalibration(lgdModel,data(TestInd,:),CorrelationType="kendall")CalMeasure=1×4 table

RSquared RMSE Correlation SampleMeanError

________ _______ ___________ _______________

Beta 0.080804 0.24112 0.29448 -0.052396

CalData=1394×4 table

Observed Predicted_Beta Residuals_Beta Weights

_________ ______________ ______________ _______

0.0064766 0.093695 -0.087218 1

0.007947 0.14915 -0.1412 1

0.063182 0.35263 -0.28944 1

0 0.096434 -0.096434 1

0.10904 0.18858 -0.079542 1

0 0.2595 -0.2595 1

0.89463 0.26767 0.62696 1

0 0.021315 -0.021315 1

0.072437 0.17736 -0.10492 1

0.036006 0.22556 -0.18955 1

0 0.13369 -0.13369 1

0.39549 0.16768 0.2278 1

0.057675 0.29159 -0.23392 1

0.014439 0.1617 -0.14726 1

0 0.10506 -0.10506 1

0 0.1161 -0.1161 1

⋮

Generate a scatter plot of the predicted and observed LGDs using modelCalibrationPlot.

modelCalibrationPlot(lgdModel,data(TestInd,:))

Input Arguments

Name-Value Arguments

Output Arguments

More About

References

[1] Baesens, Bart, Daniel Roesch, and Harald Scheule. Credit Risk Analytics: Measurement Techniques, Applications, and Examples in SAS. Wiley, 2016.

[2] Bellini, Tiziano. IFRS 9 and CECL Credit Risk Modelling and Validation: A Practical Guide with Examples Worked in R and SAS. San Diego, CA: Elsevier, 2019.

Version History

Introduced in R2023aSee Also

Tobit | Regression | Beta | modelCalibrationPlot | modelDiscriminationPlot | modelDiscrimination | predict | fitLGDModel