hwcalbyfloor

Calibrate Hull-White tree using floors

Syntax

Description

[

calibrates the Alpha,Sigma,OptimOut] = hwcalbyfloor(RateSpec,MarketStrikeMarketMaturity,MarketVolatility)Alpha (mean reversion) and Sigma

(volatility) using floor market data and the Hull-White model using the entire floor

surface.

The Hull-White calibration functions (hwcalbyfloor and hwcalbycap) support three models: Black (default), Bachelier or Normal, and

Shifted Black. For more information, see the optional arguments for

Shift and Model.

[

estimates the Alpha,Sigma,OptimOut = hwcalbyfloor(RateSpec,MarketStrikeMarketMaturity,MarketVolatility,Strike,Settle,Maturity)Alpha (mean reversion) and Sigma

(volatility) using floor market data and the Hull-White model to price a floor at a

particular maturity/volatility using the additional optional input arguments for

Strike, Settle, and

Maturity.

Strike, Settle, and

Maturity arguments are specified to calibrate to a specific point

on the market volatility surface. If omitted, the calibration is performed across all the

market instruments

For an example of calibrating using the Hull-White model with

Strike, Settle, and Maturity

input arguments, see Calibrating Hull-White Model Using Market Data.

[

adds optional name-value pair arguments. Alpha,Sigma,OptimOut] = hwcalbyfloor(___,Name,Value)

Examples

This example shows how to use hwcalbyfloor input

arguments for MarketStrike, MarketMaturity, and

MarketVolatility to calibrate the HW model using the entire floor

volatility surface.

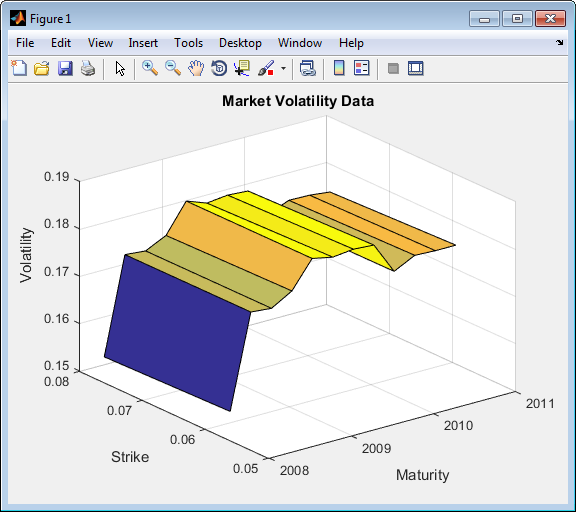

Floor market volatility data covering two strikes over 12 maturity dates.

Reset = 4; MarketStrike = [0.0590; 0.0790]; MarketMaturity = [datetime(2008,3,21) ; datetime(2008,6,21) ; datetime(2008,9,21) ; datetime(2008,12,21) ; ... datetime(2009,3,21) ; datetime(2009,6,21) ; datetime(2009,9,21) ; datetime(2009,12,21); datetime(2010,3,21) ; ... datetime(2010,6,21); datetime(2010,9,21) ; datetime(2010,12,21)]; MarketVolaltility = [0.1533 0.1731 0.1727 0.1752 0.1809 0.1800 0.1805 0.1802 ... 0.1735 0.1757 0.1755 0.1755; 0.1526 0.1730 0.1726 0.1747 0.1808 0.1792 0.1797 0.1794 ... 0.1733 0.1751 0.1750 0.1745];

Plot market volatility surface.

[AllMaturities,AllStrikes] = meshgrid(MarketMaturity,MarketStrike); figure; surf(AllMaturities,AllStrikes,MarketVolaltility) xlabel('Maturity') ylabel('Strike') zlabel('Volatility') title('Market Volatility Data')

Set interest rate term structure and create a RateSpec.

Settle = '21-Jan-2008'; Compounding = 4; Basis = 0; Rates= [0.0627; 0.0657; 0.0691; 0.0717; 0.0739; 0.0755; 0.0765; 0.0772; 0.0779; 0.0783; 0.0786; 0.0789]; EndDates = [datetime(2008,3,21) ; datetime(2008,6,21) ; datetime(2008,9,21) ; datetime(2008,12,21) ; ... datetime(2009,3,21) ; datetime(2009,6,21) ; datetime(2009,9,21) ; datetime(2009,12,21); datetime(2010,3,21) ; ... datetime(2010,6,21); datetime(2010,9,21) ; datetime(2010,12,21)]; RateSpec = intenvset('ValuationDate', Settle, 'StartDates', Settle, ... 'EndDates', EndDates,'Rates', Rates, 'Compounding', Compounding, ... 'Basis',Basis)

RateSpec =

FinObj: 'RateSpec'

Compounding: 4

Disc: [12x1 double]

Rates: [12x1 double]

EndTimes: [12x1 double]

StartTimes: [12x1 double]

EndDates: [12x1 double]

StartDates: 733428

ValuationDate: 733428

Basis: 0

EndMonthRule: 1Calibrate Hull-White model from market data.

o = optimoptions('lsqnonlin','TolFun',1e-5,'Display','off'); [Alpha, Sigma] = hwcalbyfloor(RateSpec, MarketStrike, MarketMaturity, ... MarketVolaltility, 'Reset', Reset,'Basis', Basis, 'OptimOptions', o)

Warning: LSQNONLIN did not converge to an optimal solution. It exited with exitflag = 3.

> In hwcalbycapfloor>optimizeOverCapSurface at 232

In hwcalbycapfloor at 79

In hwcalbyfloor at 81

Alpha =

0.0835

Sigma =

0.0145

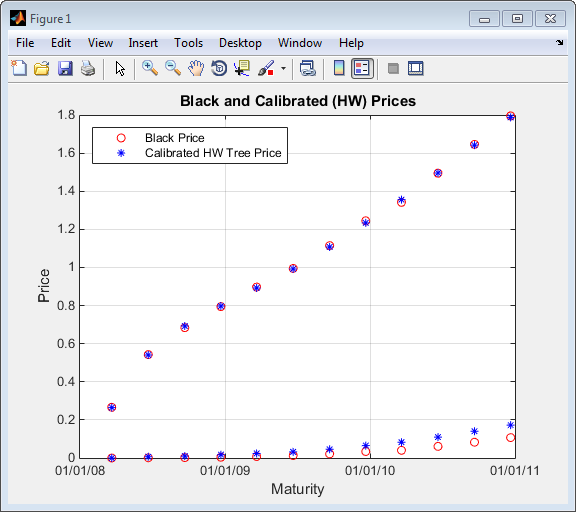

Compare with Black prices.

BlkPrices = floorbyblk(RateSpec,AllStrikes(:), Settle, AllMaturities(:), ... MarketVolaltility(:),'Reset',Reset,'Basis',Basis)

BlkPrices =

0

0.2659

0.0010

0.5426

0.0021

0.6841

0.0042

0.7947

0.0081

0.8970

0.0128

0.9947

0.0217

1.1145

0.0340

1.2448

0.0402

1.3415

0.0610

1.4947

0.0827

1.6458

0.1071

1.7951

Setup Hull-White tree using calibrated parameters, alpha, and sigma.

VolDates = EndDates; VolCurve = Sigma*ones(numel(EndDates),1); AlphaDates = EndDates; AlphaCurve = Alpha*ones(numel(EndDates),1); HWVolSpec = hwvolspec(Settle, VolDates, VolCurve, AlphaDates, AlphaCurve); HWTimeSpec = hwtimespec(Settle, EndDates, Compounding); HWTree = hwtree(HWVolSpec, RateSpec, HWTimeSpec, 'Method', 'HW2000')

HWTree =

FinObj: 'HWFwdTree'

VolSpec: [1x1 struct]

TimeSpec: [1x1 struct]

RateSpec: [1x1 struct]

tObs: [0 0.6593 1.6612 2.6593 3.6612 4.6593 5.6612 6.6593 7.6612 8.6593 9.6612 10.6593]

dObs: [733428 733488 733580 733672 733763 733853 733945 734037 734128 734218 734310 734402]

CFlowT: {1x12 cell}

Probs: {1x11 cell}

Connect: {1x11 cell}

FwdTree: {1x12 cell}Compute Hull-White prices based on the calibrated tree.

HWPrices = floorbyhw(HWTree, AllStrikes(:), Settle, AllMaturities(:), Reset, Basis)

HWPrices =

0

0.2644

0.0067

0.5404

0.0101

0.6924

0.0169

0.7974

0.0236

0.8919

0.0320

0.9919

0.0460

1.1074

0.0649

1.2340

0.0829

1.3558

0.1096

1.4957

0.1406

1.6418

0.1724

1.7877Plot Black prices against the calibrated Hull-White tree prices.

figure; plot(AllMaturities(:), BlkPrices, 'or', AllMaturities(:), HWPrices, '*b'); xtickformat; xlabel('Maturity'); ylabel('Price'); title('Black and Calibrated (HW) Prices'); legend('Black Price', 'Calibrated HW Tree Price','Location', 'NorthWest'); grid on

This example shows how to use hwcalbyfloor to calibrate market data with the Normal (Bachelier) model to price floorlets. Use the Normal (Bachelier) model to perform calibrations when working with negative interest rates, strikes, and normal implied volatilities.

Consider a floor with these parameters:

Settle = datetime(2016,12,30); Maturity = datetime(2019,12,30); Strike = -0.004075; Reset = 2; Principal = 100; Basis = 0;

The floorlets and market data for this example are defined as:

floorletDates = cfdates(Settle, Maturity, Reset, Basis); datestr(floorletDates')

ans = 6×11 char array

'30-Jun-2017'

'30-Dec-2017'

'30-Jun-2018'

'30-Dec-2018'

'30-Jun-2019'

'30-Dec-2019'

% Market data information MarketStrike = [-0.00595; 0]; MarketMat = [datetime(2017,6,30) ; datetime(2017,12,30) ; datetime(2018,6,30) ; datetime(2018,12,30) ; datetime(2019,6,30) ; datetime(2019,12,30)]; MarketVol = [0.184 0.2329 0.2398 0.2467 0.2906 0.3348; % First row in table corresponding to Strike 1 0.217 0.2707 0.2760 0.2814 0.3160 0.3508]; % Second row in table corresponding to Strike 2

Define the RateSpec using intenvset.

Rates= [-0.003210;-0.003020;-0.00182;-0.001343;-0.001075]; ValuationDate = datetime(2016,12,30); EndDates = [datetime(2017,6,30) ; datetime(2017,12,30) ; datetime(2018,6,30) ; datetime(2018,12,30) ; datetime(2019,12,30)]; Compounding = 2; Basis = 0; RateSpec = intenvset('ValuationDate', ValuationDate, ... 'StartDates', ValuationDate, 'EndDates', EndDates, ... 'Rates', Rates, 'Compounding', Compounding, 'Basis', Basis);

Use hwcalbyfloor to find values for the volatility parameters Alpha and Sigma using the Normal (Bachelier) model.

format short o=optimoptions('lsqnonlin','TolFun',100*eps); warning ('off','fininst:hwcalbycapfloor:NoConverge') [Alpha, Sigma, OptimOut] = hwcalbyfloor(RateSpec, MarketStrike, MarketMat,... MarketVol, Strike, Settle, Maturity, 'Reset', Reset, 'Principal', Principal,... 'Basis', Basis, 'OptimOptions', o, 'model', 'normal')

Local minimum possible. lsqnonlin stopped because the size of the current step is less than the value of the step size tolerance. <stopping criteria details>

Alpha = 1.0000e-06

Sigma = 0.3410

OptimOut = struct with fields:

resnorm: 1.9233e-04

residual: [5×1 double]

exitflag: 2

output: [1×1 struct]

lambda: [1×1 struct]

jacobian: [5×2 double]

The OptimOut.residual field of the OptimOut structure is the optimization residual. This value contains the difference between the Normal (Bachelier) floorlets and those calculated during the optimization. Use the OptimOut.residual value to calculate the percentual difference (error) compared to Normal (Bachelier) floorlet prices, and then decide whether the residual is acceptable. There is almost always some residual, so decide if it is acceptable to parameterize the market with a single value of Alpha and Sigma.

Price the floorlets using the market data and Normal (Bachelier) model to obtain the reference floorlet values. To determine the effectiveness of the optimization, calculate reference floorlet values using the Normal (Bachelier) formula and the market data. Note, you must first interpolate the market data to obtain the floorlets for calculation.

% MarketMatNum = datenum(MarketMat); [Mats, Strikes] = meshgrid(MarketMat, MarketStrike); MarketMat_T = yearfrac(Settle,Mats); Mats_T = yearfrac(Settle,Maturity); FlatVol = interp2(MarketMat_T, Strikes, MarketVol, Mats_T, Strike, 'spline'); % FlatVol = interp2(Mats, Strikes, MarketVol, datenum(Maturity), Strike, 'spline'); [FloorPrice, Floorlets] = floorbynormal(RateSpec, Strike, Settle, Maturity, FlatVol,... 'Reset', Reset, 'Basis', Basis, 'Principal', Principal); Floorlets = Floorlets(2:end)'

Floorlets = 5×1

4.7637

6.7180

8.1833

9.5825

10.6090

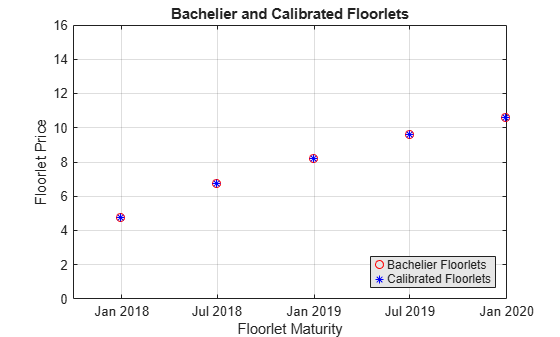

Compare the optimized values and Normal (Bachelier) values, and display the results graphically. After calculating the reference values for the floorlets, compare the values analytically and graphically to determine whether the calculated single values of Alpha and Sigma provide an adequate approximation.

OptimFloorlets = Floorlets+OptimOut.residual;

disp(' ');disp(' Bachelier Calibrated Floorlets');Bachelier Calibrated Floorlets

disp([Floorlets OptimFloorlets])

4.7637 4.7685

6.7180 6.7263

8.1833 8.1878

9.5825 9.5795

10.6090 10.6007

plot(MarketMat(2:end), Floorlets, 'or', MarketMat(2:end), OptimFloorlets, '*b'); xlabel('Floorlet Maturity'); ylabel('Floorlet Price'); ylim ([0 16]); title('Bachelier and Calibrated Floorlets'); h = legend('Bachelier Floorlets', 'Calibrated Floorlets'); set(h, 'color', [0.9 0.9 0.9]); set(h, 'Location', 'SouthEast'); set(gcf, 'NumberTitle', 'off') grid on