bssm

Description

bssm creates a bssm object, representing a Bayesian linear state-space model,

from a specified parameter-to-matrix mapping function, which defines the state-space model

structure, and the log prior distribution function of the parameters. The state-space model

can be time-invariant or time-varying (see Decide on Model Structure), and the state or observation

variables, xt or

yt, respectively, can be multivariate

series.

In general, a bssm object specifies the joint prior distribution and

characteristics of the state-space model only. That is, the model object is a template

intended for further use. Specifically, to incorporate data into the model for posterior

distribution analysis, pass the model object and data to the appropriate object function.

Alternative state-space models include:

Creation

Syntax

Description

There are several ways to create a bssm object representing a Bayesian

state-space model:

Create Prior Model — Directly create a

bssmobject, representing a prior model, by using thebssmfunction and specifying the parameter-to-matrix mapping function and log prior distribution function of the parameters. This method accommodates simple through complex state-space model structures. For more details, see the following syntax.Convert Standard Model to Bayesian Prior Model — Convert a specified standard, linear state-space model, an

ssmobject, to abssmobject by passing the model to thessm2bssmfunction. The converted Bayesian model has the same state-space structure as the standard model. Use this method for simple state-space models when you prefer to specify the coefficient matrices explicitly. You can optionally specify the log prior density of the parameters. For details, seessm2bssmandssm.Estimate Posterior Model — Pass a

bssmobject representing a prior model, observed response data, and initial parameter values to theestimatefunction to obtain abssmobject representing a posterior model. For more details, seeestimate.

PriorMdl = bssm(ParamMap,ParamDistribution)PriorMdl, representing a prior model with Gaussian state

disturbances and observation innovations, using the parameter-to-matrix mapping function

ParamMap, which you write, and the log prior distribution of the

parameters.

The ParamMap function maps the collection of linear state-space

model parameters Θ to the time-invariant or time-varying coefficient matrices

A, B, C, and

D. In addition to the coefficient matrices,

ParamMap can optionally map any of the following quantities:

Initial state means and covariances

Mean0andCov0State types

StateTypeDeflated observation data

DeflatedDatato accommodate a regression component in the observation equation

The ParamDistribution function accepts Θ and returns the

corresponding log density.

PriorMdl is a template that specifies the joint prior distribution

of Θ and the structure of the state-space model.

PriorMdl = bssm(ParamMap,ParamDistribution,Name=Value)bssm(ParamMap,ParamDistribution,ObservationDistribution=struct("Name","t","DoF",6))

specifies t distribution with 6 degrees of freedom for all observation

innovation variables ut in the Bayesian

state-space model.

Input Arguments

Properties

Object Functions

Examples

Create a Bayesian state-space model containing two independent, stationary, autoregressive states. The observations are the deterministic sum of the two states (in other words, the model does not impose observation errors ). Symbolically, the system of equations is

Arbitrarily assume that the prior distribution of , , , and are independent Gaussian random variables with mean 0.5 and variance 1.

The Local Functions section contains two functions required to specify the Bayesian state-space model. You can use the functions only within this script.

The paramMap function accepts a vector of the unknown state-space model parameters and returns all of the following quantities:

A= .B= .C= .D= 0.Mean0andCov0are empty arrays[], which specify the defaults.StateType= , indicating that each state is stationary.

The paramDistribution function accepts the same vector of unknown parameters as does paramMap, but it returns the log prior density of the parameters at their current values. Specify that parameter values outside the parameter space have log prior density of -Inf.

Create the Bayesian state-space model by passing function handles directly to paramMap and paramDistribution to bssm.

Mdl = bssm(@paramMap,@priorDistribution)

Mdl =

Mapping that defines a state-space model:

@paramMap

Log density of parameter prior distribution:

@priorDistribution

Mdl is a bssm model specifying the state-space model structure and prior distribution of the state-space model parameters. Because Mdl contains unknown values, it serves as a template for posterior estimation.

Local Functions

This example uses the following functions. paramMap is the parameter-to-matrix mapping function and priorDistribution is the log prior distribution of the parameters.

function [A,B,C,D,Mean0,Cov0,StateType] = paramMap(theta) A = [theta(1) 0; 0 theta(2)]; B = [theta(3) 0; 0 theta(4)]; C = [1 1]; D = 0; Mean0 = []; % MATLAB uses default initial state mean Cov0 = []; % MATLAB uses initial state covariances StateType = [0; 0]; % Two stationary states end function logprior = priorDistribution(theta) paramconstraints = [(abs(theta(1)) >= 1) (abs(theta(2)) >= 1) ... (theta(3) < 0) (theta(4) < 0)]; if(sum(paramconstraints)) logprior = -Inf; else mu0 = 0.5*ones(numel(theta),1); sigma0 = 1; p = normpdf(theta,mu0,sigma0); logprior = sum(log(p)); end end

Create a time-varying, Bayesian state-space model with these characteristics:

From periods 1 through 250, the state equation includes stationary AR(2) and MA(1) models, respectively, and the observation model is the weighted sum of the two states.

From periods 251 through 500, the state model includes only the first AR(2) model.

and is the identity matrix.

The prior density is flat.

Symbolically, the state-space model is

Write a function that specifies how the parameters theta map to the state-space model matrices, the initial state moments, and the state types. Save this code as a file named timeVariantParamMap.m on your MATLAB® path. Alternatively, open the example to access the function.

function [A,B,C,D,Mean0,Cov0,StateType] = timeVariantParamMapBayes(theta,T) % Time-variant, Bayesian state-space model parameter mapping function % example. This function maps the vector params to the state-space matrices % (A, B, C, and D), the initial state value and the initial state variance % (Mean0 and Cov0), and the type of state (StateType). From periods 1 % through T/2, the state model is a stationary AR(2) and an MA(1) model, % and the observation model is the weighted sum of the two states. From % periods T/2 + 1 through T, the state model is the AR(2) model only. The % log prior distribution enforces parameter constraints (see % flatPriorBSSM.m). T1 = floor(T/2); T2 = T - T1 - 1; A1 = {[theta(1) theta(2) 0 0; 1 0 0 0; 0 0 0 theta(4); 0 0 0 0]}; B1 = {[theta(3) 0; 0 0; 0 1; 0 1]}; C1 = {theta(5)*[1 0 1 0]}; D1 = {theta(6)}; Mean0 = [0.5 0.5 0 0]; Cov0 = eye(4); StateType = [0 0 0 0]; A2 = {[theta(1) theta(2) 0 0; 1 0 0 0]}; B2 = {[theta(3); 0]}; A3 = {[theta(1) theta(2); 1 0]}; B3 = {[theta(3); 0]}; C3 = {theta(7)*[1 0]}; D3 = {theta(8)}; A = [repmat(A1,T1,1); A2; repmat(A3,T2,1)]; B = [repmat(B1,T1,1); B2; repmat(B3,T2,1)]; C = [repmat(C1,T1,1); repmat(C3,T2+1,1)]; D = [repmat(D1,T1,1); repmat(D3,T2+1,1)]; end

Write a function that specifies a joint flat prior and parameter constraints. Save this code as a file named flatPriorBSSM.m on your MATLAB path. Alternatively, open the example to access the function.

function logprior = flatPriorBSSM(theta) % flatPriorBSSM computes the log of the flat prior density for the eight % variables in theta (see timeVariantParamMapBayes.m). Log probabilities % for parameters outside the parameter space are -Inf. % theta(1) and theta(2) are lag 1 and lag 2 terms in a stationary AR(2) % model. The eigenvalues of the AR(1) representation need to be within % the unit circle. evalsAR2 = eig([theta(1) theta(2); 1 0]); evalsOutUC = sum(abs(evalsAR2) >= 1) > 0; % Standard deviations of disturbances and errors (theta(3), theta(6), % and theta(8)) need to be positive. nonnegsig1 = theta(3) <= 0; nonnegsig2 = theta(6) <= 0; nonnegsig3 = theta(8) <= 0; paramconstraints = [evalsOutUC nonnegsig1 ... nonnegsig2 nonnegsig3]; if sum(paramconstraints) > 0 logprior = -Inf; else logprior = 0; % Prior density is proportional to 1 for all values % in the parameter space. end end

Create a bssm object representing the Bayesian state-space model object. Supply the parameter-to-matrix mapping function timeVariantParamMapBayes as a function handle of solely theta by setting the time series length to 500.

numObs = 500; Mdl = bssm(@(theta)timeVariantParamMapBayes(theta,numObs),@flatPriorBSSM)

Mdl =

Mapping that defines a state-space model:

@(theta)timeVariantParamMapBayes(theta,numObs)

Log density of parameter prior distribution:

@flatPriorBSSM

This example shows how to specify that the state disturbances of a Bayesian state-space model are Student's t distributed in order to model excess kurtosis in the state equation. The example shows how to prepare the degrees of freedom parameter for posterior estimation and the example fully specifies the distribution.

Consider the Bayesian state-space model in Create Time-Invariant Bayesian State-Space Model with Known and Unknown Parameters, but assume that the state disturbances are distributed as a Student's random variable.

Create the model by passing function handles to the local functions that represent the state-space model structure and prior distribution of the model parameters . Specify that the distribution of the state disturbances is Student's .

Mdl = bssm(@paramMap,@priorDistribution,StateDistribution="t");

Mdl.StateDistributionans = struct with fields:

Name: "t"

DoF: NaN

Mdl is a bssm model. The property Mdl.StateDistribution is a structure array specifying the distribution of the state disturbances. The field DoF is NaN by default, which means that the -distribution degrees of freedom is configured for estimation with all unknown state-space model parameters .

You can specify a fixed value for the degrees of freedom two ways:

By setting the DoF field to the positive scalar using dot notation

By recreating the

bssmmodel and supplying a structure array specifying the distribution name and degrees of freedom

Specify that the degrees of freedom is 6 by using both methods.

Mdl.StateDistribution.DoF = 6

Mdl =

Mapping that defines a state-space model:

@paramMap

Log density of parameter prior distribution:

@priorDistribution

Degree of freedom of t distribution in the state equation:

6

statedist = struct("Name","t","DoF",6); Mdl2 = bssm(@paramMap,@priorDistribution,StateDistribution=statedist)

Mdl2 =

Mapping that defines a state-space model:

@paramMap

Log density of parameter prior distribution:

@priorDistribution

Degree of freedom of t distribution in the state equation:

6

Mdl and Mdl2 are equal.

Local Functions

function [A,B,C,D,Mean0,Cov0,StateType] = paramMap(theta) A = [theta(1) 0; 0 theta(2)]; B = [theta(3) 0; 0 theta(4)]; C = [1 1]; D = 0; Mean0 = []; % MATLAB uses default initial state mean Cov0 = []; % MATLAB uses initial state covariances StateType = [0; 0]; % Two stationary states end function logprior = priorDistribution(theta) paramconstraints = [(abs(theta(1)) >= 1) (abs(theta(2)) >= 1) ... (theta(3) < 0) (theta(4) < 0)]; if(sum(paramconstraints)) logprior = -Inf; else mu0 = 0.5*ones(numel(theta),1); sigma0 = 1; p = normpdf(theta,mu0,sigma0); logprior = sum(log(p)); end end

To model volatility clustering, you can specify distributed observation innovations by setting appropriate mixture weights, and regime means and variances of a 7-regime Gaussian mixture distribution.

Consider the Bayesian state-space model in Create Time-Invariant Bayesian State-Space Model with Known and Unknown Parameters, but assume that the observation-innovations process is distributed as a random variable.

Create a structure array with the following fields and values.

Field

Namewith value"mixture"Field

Weightwith value[0.0089 0.0541 0.1338 0.2761 0.2923 0.1494 0.0854]Field

Meanwith value[-9.3202 -5.3145 -3.4147 -1.7097 -0.4531 0.3975 1.1925]Field

Variancewith value[3.2793 2.4574 1.8874 1.3121 0.8843 0.5898 0.4995].^2

weight = [0.0089 0.0541 0.1338 0.2761 0.2923 0.1494 0.0854]; mu = [-9.3202 -5.3145 -3.4147 -1.7097 -0.4531 0.3975 1.1925]; sigma2 = [3.2793 2.4574 1.8874 1.3121 0.8843 0.5898 0.4995].^2; ObsInnovDist = struct("Name","mixture","Weight",weight, ... "Mean",mu,"Variance",sigma2);

Create the model by passing function handles to the local functions that represent the state-space model structure and prior distribution of the model parameters . Use the structure array ObsInnovDist to specify that the distribution of the observation innovations is finite Gaussian mixture with hyperparameters that define a distribution.

Mdl = bssm(@paramMap,@priorDistribution,ObservationDistribution=ObsInnovDist); Mdl.ObservationDistribution

ans = struct with fields:

Name: "mixture"

Weight: [0.0089 0.0541 0.1338 0.2761 0.2923 0.1494 0.0854]

Mean: [-9.3202 -5.3145 -3.4147 -1.7097 -0.4531 0.3975 1.1925]

Variance: [10.7538 6.0388 3.5623 1.7216 0.7820 0.3479 0.2495]

Mdl is a bssm model. The property Mdl.ObservationDistribution is a structure array specifying the distribution of the observation-innovations process. All distribution hyperparameters are fully specified.

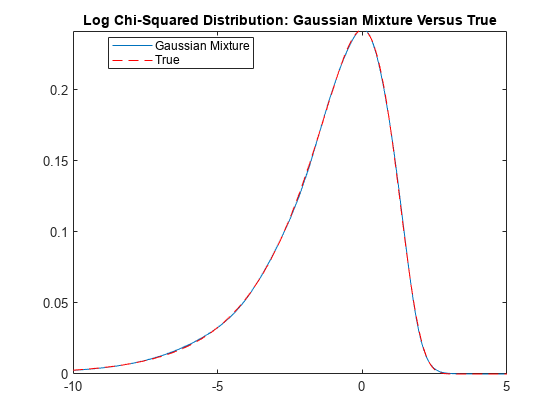

Plot the distribution of the observation innovations. Compare the Gaussian mixture representation of the and the true distributions.

r = numel(weight); LogChi2GMMdl = gmdistribution(mu',reshape(sigma2,1,1,r),weight); gmPDF = @(x)arrayfun(@(x0)pdf(LogChi2GMMdl,x0),x); logchi2PDF = @(x)((1/sqrt(2*pi))*exp((x-exp(x))/2)); figure fplot(gmPDF,[-10,5]) hold on fplot(logchi2PDF,"--r") title("Log Chi-Squared Distribution: Gaussian Mixture Versus True") legend("Gaussian Mixture","True",Location="best")

The distributions appear nearly identical.

Local Functions

function [A,B,C,D,Mean0,Cov0,StateType] = paramMap(theta) A = [theta(1) 0; 0 theta(2)]; B = [theta(3) 0; 0 theta(4)]; C = [1 1]; D = 0; Mean0 = []; % MATLAB uses default initial state mean Cov0 = []; % MATLAB uses initial state covariances StateType = [0; 0]; % Two stationary states end function logprior = priorDistribution(theta) paramconstraints = [(abs(theta(1)) >= 1) (abs(theta(2)) >= 1) ... (theta(3) < 0) (theta(4) < 0)]; if(sum(paramconstraints)) logprior = -Inf; else mu0 = 0.5*ones(numel(theta),1); sigma0 = 1; p = normpdf(theta,mu0,sigma0); logprior = sum(log(p)); end end

Consider a regression of the US unemployment rate onto and real gross national product (RGNP) rate, and suppose the resulting innovations are an ARMA(1,1) process. The state-space form of the relationship is

where:

is the ARMA process.

is a dummy state for the MA(1) effect.

is the observed unemployment rate deflated by a constant and the RGNP rate ().

is an iid Gaussian series with mean 0 and standard deviation 1.

Load the Nelson-Plosser data set, which contains a table DataTable that has the unemployment rate and RGNP series, among other series.

load Data_NelsonPlosserCreate a variable in DataTable that represents the returns of the raw RGNP series. Because price-to-returns conversion reduces the sample size by one, prepad the series with NaN.

DataTable.RGNPRate = [NaN; price2ret(DataTable.GNPR)]; T = height(DataTable);

Create variables for the regression. Represent the unemployment rate as the observation series and the constant and RGNP rate series as the deflation data .

Z = [ones(T,1) DataTable.RGNPRate]; y = DataTable.UR;

Write a function that specifies how the parameters theta map to the state-space model matrices, defers the initial state moments to the default, specifies the state types, and specifies the regression. Save this code as a file named armaDeflateYBayes.m on your MATLAB® path. Alternatively, open this example to access the function.

function [A,B,C,D,Mean0,Cov0,StateType,DeflatedY] = armaDeflateYBayes(theta,y,Z) % Time-invariant, Bayesian state-space model parameter mapping function % example. This function maps the vector parameters to the state-space % matrices (A, B, C, and D), the default initial state value and the % default initial state variance (Mean0 and Cov0), the type of state % (StateType), and the deflated observations (DeflatedY). The log prior % distribution enforces parameter constraints (see flatPriorDeflateY.m). A = [theta(1) theta(2); 0 0]; B = [1; 1]; C = [theta(3) 0]; D = 0; Mean0 = []; Cov0 = []; StateType = [0 0]; DeflatedY = y - Z*[theta(4); theta(5)]; end

Write a function that specifies a joint flat prior and parameter constraints. Save this code as a file named flatPriorDeflateY.m on your MATLAB path. Alternatively, open this example to access the function.

% Copyright 2022 The MathWorks, Inc. function logprior = flatPriorDeflateY(theta) % flatPriorDeflateY computes the log of the flat prior density for the five % variables in theta (see armaDeflateYBayes.m). Log probabilities % for parameters outside the parameter space are -Inf. % theta(1) and theta(2) are the AR and MA terms in a stationary % ARMA(1,1) model. The AR term must be within the unit circle. AROutUC = abs(theta(1)) >= 1; % The standard deviation of innovations (theta(3)) must be positive. nonnegsig1 = theta(3) <= 0; paramconstraints = [AROutUC nonnegsig1]; if sum(paramconstraints) > 0 logprior = -Inf; else logprior = 0; % Prior density is proportional to 1 for all values % in the parameter space. end end

Create a bssm object representing the Bayesian state-space model. Specify the parameter-to-matrix mapping function as a handle to a function solely of the parameters theta.

Mdl = bssm(@(theta)armaDeflateYBayes(theta,y,Z),@flatPriorDeflateY)

Mdl =

Mapping that defines a state-space model:

@(theta)armaDeflateYBayes(theta,y,Z)

Log density of parameter prior distribution:

@flatPriorDeflateY

More About

Tips

Load the data to the MATLAB workspace before creating the model.

Create the parameter-to-matrix mapping function and log prior distribution function each as their own file.

To specify a log χ21 distribution for the observation innovation process εt, set the

ObservationDistributionto the structure arraystruct("Weight",, where:weight,"Mean",mu,"Variance",sigma2)weight[0.0089 0.0541 0.1338 0.2761 0.2923 0.1494 0.0854].mu[-9.3202 -5.3145 -3.4147 -1.7097 -0.4531 0.3975 1.1925].sigma2[3.2793 2.4574 1.8874 1.3121 0.8843 0.5898 0.4995].^2.