impulse

Generate univariate ARIMA model impulse response function (IRF)

Description

y = impulse(Mdl)impulse returns the dynamic

responses starting at period 0, during which impulse applies a

unit shock to the innovation.

impulse(___) plots a discrete stem plot of the IRF of

the input ARIMA model to the current axes, using any of the input argument combinations in

the previous syntaxes.

impulse(

plots on the axes specified by ax,___)ax instead of

the current axes (gca). ax can precede any of the input

argument combinations in the previous syntaxes. (since R2024a)

[___, plots the IRF and additionally returns handles to the plotted graphics objects. Use elements of h]

= impulse(___)h to modify properties of the plot after you create it. (since R2024a)

Examples

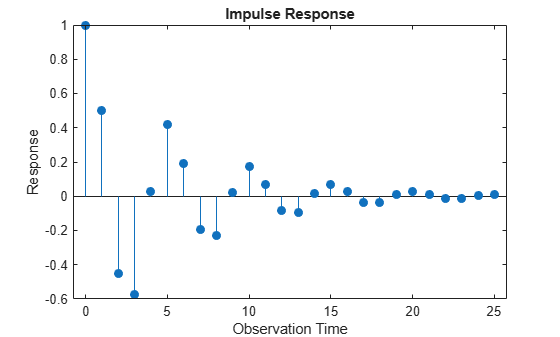

Create the AR(2) model

where is a standard Gaussian process.

Mdl = arima('AR',{0.5,-0.7},'Constant',0)

Mdl =

arima with properties:

Description: "ARIMA(2,0,0) Model (Gaussian Distribution)"

SeriesName: "Y"

Distribution: Name = "Gaussian"

P: 2

D: 0

Q: 0

Constant: 0

AR: {0.5 -0.7} at lags [1 2]

SAR: {}

MA: {}

SMA: {}

Seasonality: 0

Beta: [1×0]

Variance: NaN

Plot the IRF of .

impulse(Mdl)

The IRF has length 26; it begins at period 0, during which impulse applies a unit shock to the innovation, and ends at period 25. impulse computes the IRF by inverting the underlying AR lag operator polynomial. The length of the IRF is 26 because the dynamic multipliers beyond period 25 are below the division algorithm tolerances.

The model is stationary; the impulse response function decays with a sinusoidal pattern.

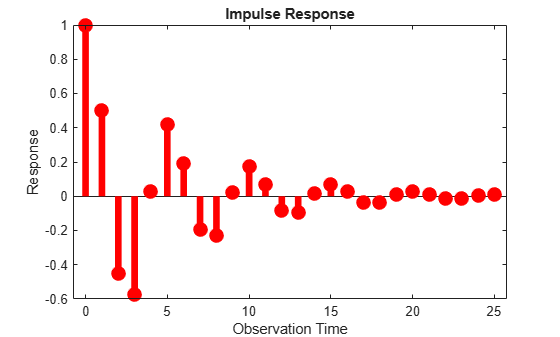

You can change characteristics of the plot by adjusting the properties of the underlying stem plot. The axes handle object stores the stem plot handle in the Children property.

Increase the line thickness (the default is 0.5). Also, change the color of the stem plot to red by using the RGB color value.

h = gca; % Current axes handle

stemh = h.Children;

stemh.LineWidth = 5;

stemh.Color = [1 0 0];

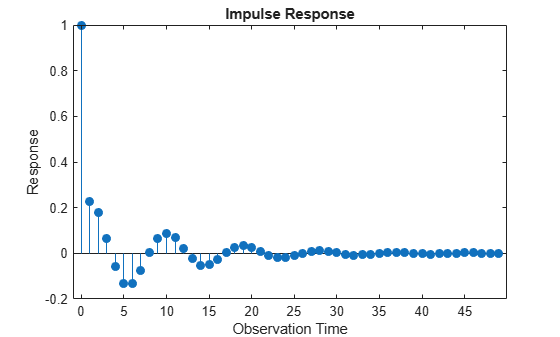

Load the quarterly US GDP data set.

load Data_GDPFor details on the data, enter Description at the command line.

Compute the GDP growth rate.

y = price2ret(Data);

Consider an ARMA(2,2) model for the GDP rate series. Create an arima model template for estimation.

Mdl = arima(2,0,2)

Mdl =

arima with properties:

Description: "ARIMA(2,0,2) Model (Gaussian Distribution)"

SeriesName: "Y"

Distribution: Name = "Gaussian"

P: 2

D: 0

Q: 2

Constant: NaN

AR: {NaN NaN} at lags [1 2]

SAR: {}

MA: {NaN NaN} at lags [1 2]

SMA: {}

Seasonality: 0

Beta: [1×0]

Variance: NaN

NaN values in properties are placeholders for estimable model parameters.

Fit the model to the entire series.

EstMdl = estimate(Mdl,y)

ARIMA(2,0,2) Model (Gaussian Distribution):

Value StandardError TStatistic PValue

__________ _____________ __________ __________

Constant 0.0036702 0.00058179 6.3085 2.8179e-10

AR{1} 1.372 0.089005 15.415 1.3022e-53

AR{2} -0.8069 0.069497 -11.611 3.6376e-31

MA{1} -1.1432 0.10159 -11.253 2.2446e-29

MA{2} 0.67355 0.08512 7.9129 2.514e-15

Variance 8.3071e-05 5.9331e-06 14.001 1.5324e-44

EstMdl =

arima with properties:

Description: "ARIMA(2,0,2) Model (Gaussian Distribution)"

SeriesName: "Y"

Distribution: Name = "Gaussian"

P: 2

D: 0

Q: 2

Constant: 0.00367019

AR: {1.37199 -0.806901} at lags [1 2]

SAR: {}

MA: {-1.14315 0.673549} at lags [1 2]

SMA: {}

Seasonality: 0

Beta: [1×0]

Variance: 8.30707e-05

The estimated AR(2) model of the GDP rate series is

where is a Gaussian series with mean 0 and variance 0.00008.

Compute the IRF of the estimated model for 50 periods.

impulse(EstMdl,50)

The dynamic response to the initial innovation shock dissipates after about 35 quarters.

Create the ARMA(1,1) model

Mdl = arima('AR',0.7,'MA',0.2,'Constant',0);

Return the IRF for 15 periods.

numObs = 15; periods = 0:(numObs-1); y = impulse(Mdl,numObs); irf = table(periods',y,'VariableNames',["Period" "y"])

irf=15×2 table

Period y

______ ________

0 1

1 0.9

2 0.63

3 0.441

4 0.3087

5 0.21609

6 0.15126

7 0.10588

8 0.074119

9 0.051883

10 0.036318

11 0.025423

12 0.017796

13 0.012457

14 0.00872

y(0), which is the dynamic response of the system at the time impulse shocks the innovation, is 1.

Input Arguments

Output Arguments

More About

Tips

To improve performance of the filtering algorithm, specify the number of periods to include in the IRF

numObs. When you do not specifynumObs,impulsecomputes the IRF by using the lag operator polynomial division algorithm, which is relatively slow, to represent the input modelMdlas a truncated, infinite-degree, moving average model. The length of the resulting IRF is generally unknown.

Alternative Functionality

The armairf function generates or plots the IRF of an

ARMA process specified by input AR and MA lag operator polynomial coefficients.

References

[1] Box, George E. P., Gwilym M. Jenkins, and Gregory C. Reinsel. Time Series Analysis: Forecasting and Control. 3rd ed. Englewood Cliffs, NJ: Prentice Hall, 1994.

[2] Enders, Walter. Applied Econometric Time Series. Hoboken, NJ: John Wiley & Sons, Inc., 1995.

[3] Hamilton, James D. Time Series Analysis. Princeton, NJ: Princeton University Press, 1994.

[4] Lütkepohl, Helmut. New Introduction to Multiple Time Series Analysis. New York, NY: Springer-Verlag, 2007.

[5] Wold, Herman. "A Study in the Analysis of Stationary Time Series." Journal of the Institute of Actuaries 70 (March 1939): 113–115. https://doi.org/10.1017/S0020268100011574.