Simulate Conditional Mean and Variance Models

This example shows how to simulate responses and conditional variances from a composite conditional mean and variance model.

Load Data and Fit Model

Load the NASDAQ data included with the toolbox. Fit a conditional mean and variance model to the daily returns. Scale the returns to percentage returns for numerical stability

load Data_EquityIdx nasdaq = DataTable.NASDAQ; r = 100*price2ret(nasdaq); T = length(r); Mdl = arima('ARLags',1,'Variance',garch(1,1),... 'Distribution','t'); EstMdl = estimate(Mdl,r,'Variance0',{'Constant0',0.001});

ARIMA(1,0,0) Model (t Distribution):

Value StandardError TStatistic PValue

________ _____________ __________ __________

Constant 0.093488 0.016694 5.6002 2.1414e-08

AR{1} 0.13911 0.018857 7.3771 1.6175e-13

DoF 7.4775 0.88262 8.472 2.4126e-17

GARCH(1,1) Conditional Variance Model (t Distribution):

Value StandardError TStatistic PValue

________ _____________ __________ __________

Constant 0.011246 0.0036305 3.0976 0.0019511

GARCH{1} 0.90766 0.010516 86.316 0

ARCH{1} 0.089897 0.010835 8.2966 1.0711e-16

DoF 7.4775 0.88262 8.472 2.4126e-17

[e0,v0] = infer(EstMdl,r);

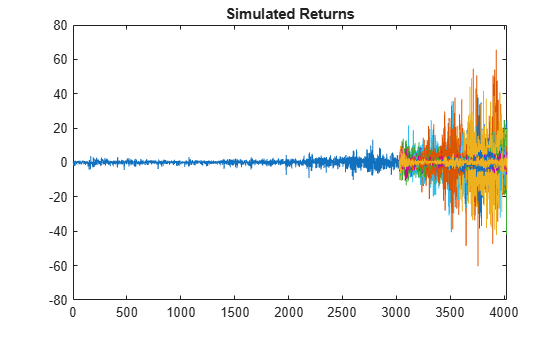

Simulate Returns, Innovations, and Conditional Variances

Use simulate to generate 100 sample paths for the returns, innovations, and conditional variances for a 1000-period future horizon. Use the observed returns and inferred residuals and conditional variances as presample data.

rng 'default'; [y,e,v] = simulate(EstMdl,1000,'NumPaths',100,... 'Y0',r,'E0',e0,'V0',v0); figure plot(r) hold on plot(T+1:T+1000,y) xlim([0,T+1000]) title('Simulated Returns') hold off

The simulation shows increased volatility over the forecast horizon.

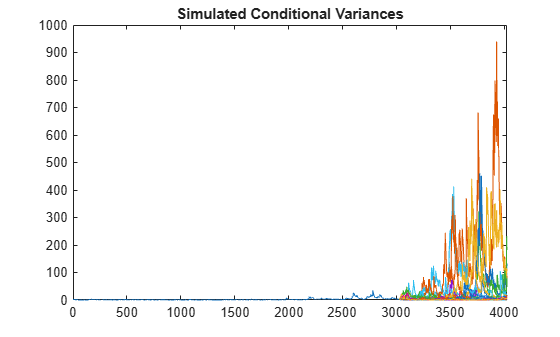

Plot Conditional Variances

Plot the inferred and simulated conditional variances.

figure plot(v0) hold on plot(T+1:T+1000,v) xlim([0,T+1000]) title('Simulated Conditional Variances') hold off

The increased volatility in the simulated returns is due to larger conditional variances over the forecast horizon.

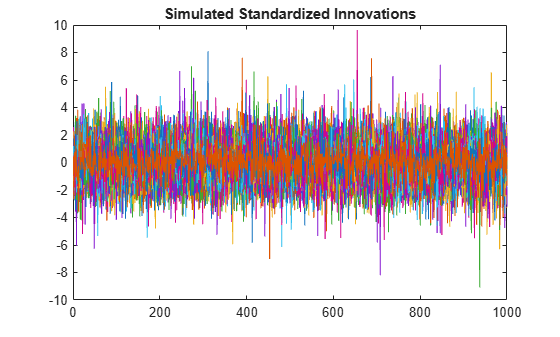

Plot Standardized Innovations

Standardize the innovations using the square root of the conditional variance process. Plot the standardized innovations over the forecast horizon.

figure

plot(e./sqrt(v))

xlim([0,1000])

title('Simulated Standardized Innovations')

The fitted model assumes the standardized innovations follow a standardized Student's distribution. Thus, simulate generates more innovations at the distribution tails than is expected from a Gaussian data-generating process.

See Also

arima | estimate | infer | simulate

Topics

- Specify Conditional Mean and Variance Models

- Estimate Conditional Mean and Variance Model

- Forecast Conditional Mean and Variance Model

- Volatility Modeling for Soft Commodities

- Monte Carlo Simulation of Conditional Mean Models

- Presample Data for Conditional Mean Model Simulation

- Forecast Conditional Mean Model Programmatically